Understanding Canada’s Exports and Imports by product and service and by country

What products does Canada Import and Export? Which countries, other than the United States, are important trading partners of Canada? What products is Canada a net exporter of and what is it a net importer of? The sometimes surprising answers are provided below in a brief and graphical format.

What does Canada Export?

As a country, Canada imports goods and services that amount to $1,029 billion per year or about 33% of GDP. That would not be sustainable unless exports were at a roughly similar level, which, luckily, they are. Exports in 2024 were $999 billion or about 32% of GDP. Total In a sense it can be said that every country that imports things needs to export something to pay for those imports – unless the country collectively is to run down its savings or run up its debts to pay for imports.

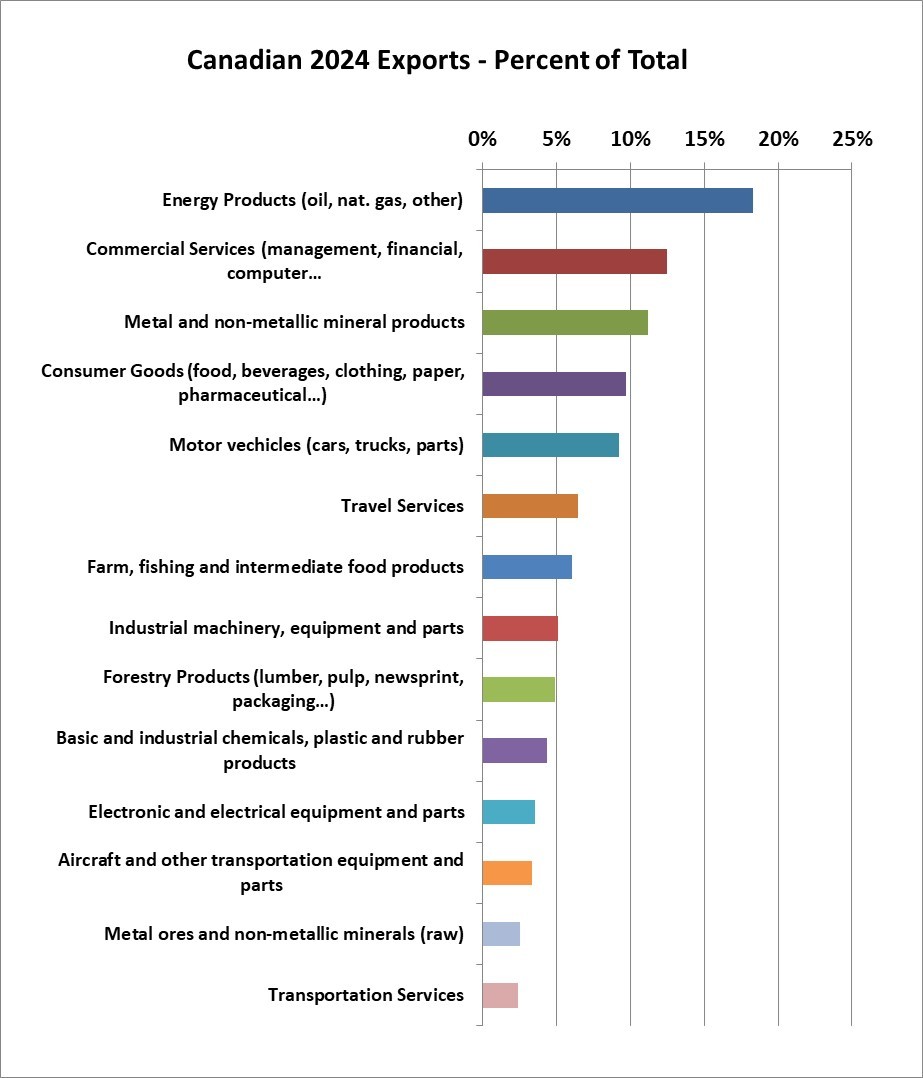

Here is a breakdown of Canada’s exports by category:

Data Source: Statistics Canada

Exports and imports of goods and services quarterly (choose current dollars, not chained 2017)

Canada’s largest category of exports by far is energy products at $183 billion or 18% of the total – crude oil is the great majority of this followed by natural gas then refined petroleum products and coal and a minor amount of electricity and nuclear fuel. Commercial services which includes management services, financial services and information services is the second largest category at $125 billion or 12.5% of the total. Metal and non-metallic mineral products is the third biggest export category at $112 billion or 11%. Consumer goods, perhaps surprisingly, is fourth largest at $97 billion or 10% of the total. Motor vehicles have declined to the fifth largest export segment at $93 billion or 9% of total exports.

Canada has a reputation for exporting relatively unprocessed natural resources. That is certainly true in regards to oil and metal and mineral ores. But most of Canada’s exports are not raw materials. For example, under forestry products, raw logs represent only 1% of that category.

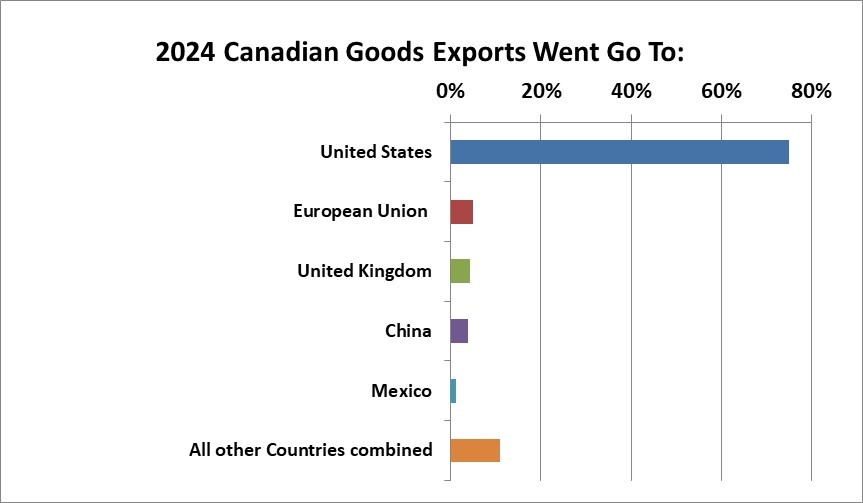

To Which Countries Does Canada Export to (Excludes Services)?

The answer to that question is alarming especially in light of the current tariff war:

Data Source, Statistics Canada

International merchandise trade for all countries and by principal trading partners, quarterly seasonally adjusted (multiply by four to annualise).

http://www.statcan.gc.ca/tables-tableaux/sum-som/l01/cst01/gblec02a-eng.htm (monthly)

Note that our data source does not include services in the exports-by-country data.

The United States accounted for the great majority of Canadian goods (merchandise) exports at $604 billion or a staggering 75% of the total. (Our figures are based on Q4 seasonally adjusted and annualized.) The European Union collectively is the second largest export destination at $39 billion or 5% of the total. The U.K. and China at about $32 billion each represent about 4% of the total. Mexico, despite its proximity imports only about $9 billion annually of goods from Canada or 1% of Canada’s total exports.

Things may be changing and China is an important “customer” country for Canada. But the fact is, for now, when it comes to Canadian exports, the United States remains our number one export destination by far. Mexico, despite its proximity accounts for only $9 billion annually or 1.2%. Canada’s exports to all but a tiny handful of countries are almost insignificant. Treating the European Union collectively, you can literally count all of Canada’s important trading destination countries on the fingers of one hand. The extent of the reliance on exports to the U.S. is sobering and, given their increasing “America-First” rhetoric and policies, alarming.

What Does Canada Import?

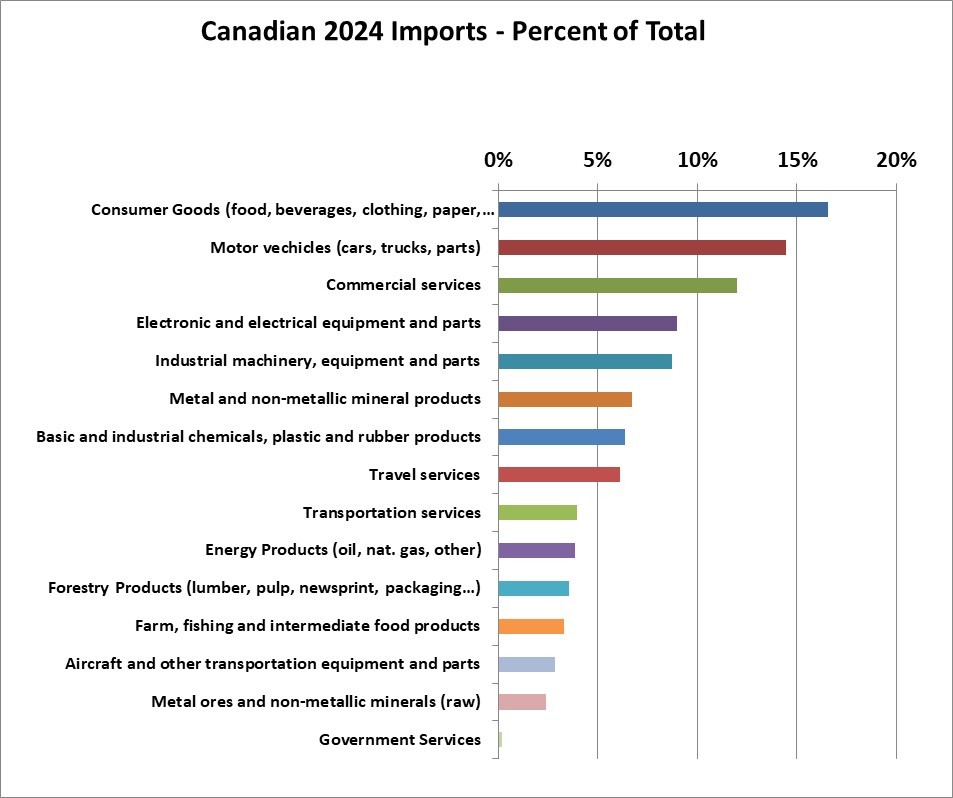

Canadian Imports by Category:

In 2023 Canada’s imports of goods and services at $946 billion were about 33% as large as its GDP.

The following chart shows imports by industry segment as a percentage of total goods and services imports.

Data Source: Statistics Canada

https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=1210013401

The data indicates that consumer goods are Canada’s largest import category at $166 billion or 17% of the total. Motor vehicles and parts at $142 billion constituted 14.5% of total goods and services imports. Commercial services constitutes $120 billion or 12% of the total.

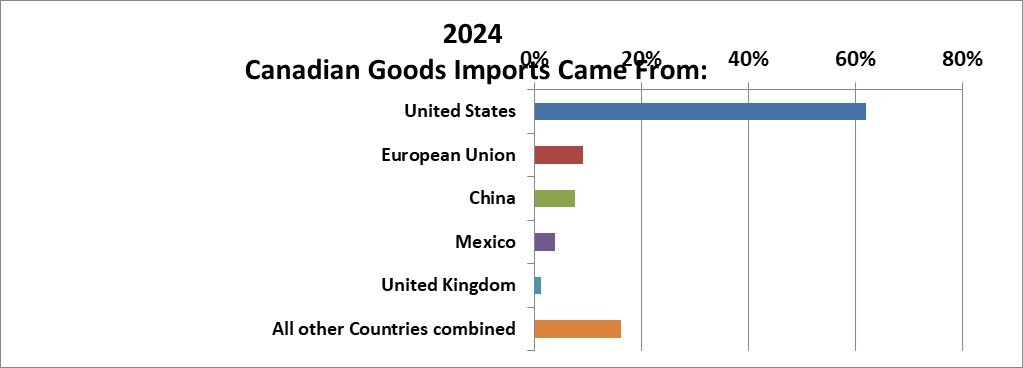

From Which Countries Does Canada Import Goods?

Data Source, Statistics Canada

Note that our data source does not include services in the imports-by-country data.

The United States accounts for $499 billion or 62% of Canada’s annual goods imports. The European Union collectively accounts for $73 billion or 9%. China accounts for $62 billion or just 8% of the total. Mexico accounts for for $31 billion or 4%% and the U.K for $10 billion or just 1%. The remaining $130 billion or 16% is spread widely around the globe. Most of the other countries in the world are insignificant to Canada in terms of imports. But there may be some countries from which Canada imports more than Mexico and certainly the U.K. This is the way our data source breaks down the countries.

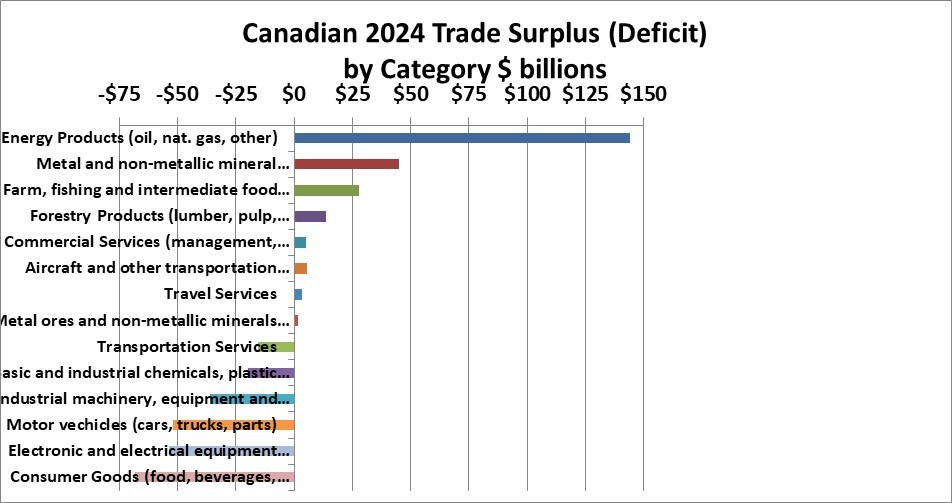

For Which Products and Services is Canada a Net Exporter and For Which a Net Importer?

Energy – largely crude oil – is Canada’s largest NET export (exports minus imports) at $144 billion. And it’s “no contest”. That’s 3.4 times larger than the next highest net export category which is “metal and non-metallic mineral products” – which includes steel and aluminum products at $45 billion. Oil is “bringing home the bacon” to this country and in a sense provides the dollars to pay for the things that Canada imports. Metal products, farm, fishing and intermediate food as well as forestry also bring home some bacon to this country.

Canada is a net exporter of commodities including notably energy products, metal & mineral products, farm, fishing & intermediate food products, and forestry products.

Canada is a net importer in most manufactured and finished goods categories including consumer goods, motor vehicles & parts, industrial machinery, and electronic & electrical equipment. Given all the support to that industry, it might be a surprise to see that motor vehicles are a large net IMPORT category for Canada.

Canadians don’t actually operate as one giant sort of “team”. But it can be argued or observed from this data that, for the country as a whole, the net exports of energy (oil) in particular and to a lesser extent other commodity products are what pay the bills to allow the country to be very much a net importer of consumer and manufactured goods.

The net contribution or surplus on energy products (mostly oil) is staggeringly large as indicated in the chart just above.

END

Shawn Allen, CFA, CPA, MBA, P.Eng.

President, InvestorsFriend Inc.

Article originally created November 3, 2007, the latest annual update was March 4, 2025.

Send any questions about this article to shawn@investorsfriend.com

Which Industries Contribute Most to Canada’s GDP?

Canada’s GDP by Industry

Which industries contribute the most to Canada’s economy? In terms of Gross Domestic Product (GDP) what are the percentages from oil and gas, real estate, construction, government services, forestry, farming, financial services and manufacturing etc.? The answers below might surprise or even shock you.

Firstly, what is the meaning of GDP?

GDP or Gross Domestic Product refers to the total dollar value of recorded economic production within a country. It measures the final value of all goods and services produced. The GDP of a particular industry is (roughly) the value of its sales minus the costs of goods or services purchased from other entities. The GDP of a particular industry measures the economic activity directly generated by that industry. The GDP of a particular industry is not a measure of its profit or value added since it does not deduct the cost of labour from the value of sales.

GDP is often criticized because it does not include the value of unpaid work or of unreported economic activities such as the “underground economy” or the value of “do-it-yourself” labour. Nevertheless, GDP is the best available figure for use in understanding the economy and the relative importance of each industry to the economy. There is one strange exception to the rule of not including unpaid and unreported economic activities. GDP includes a significant amount for the “imputed” rental value of owner-occupied houses.

What is Canada’s GDP by industry or sector?

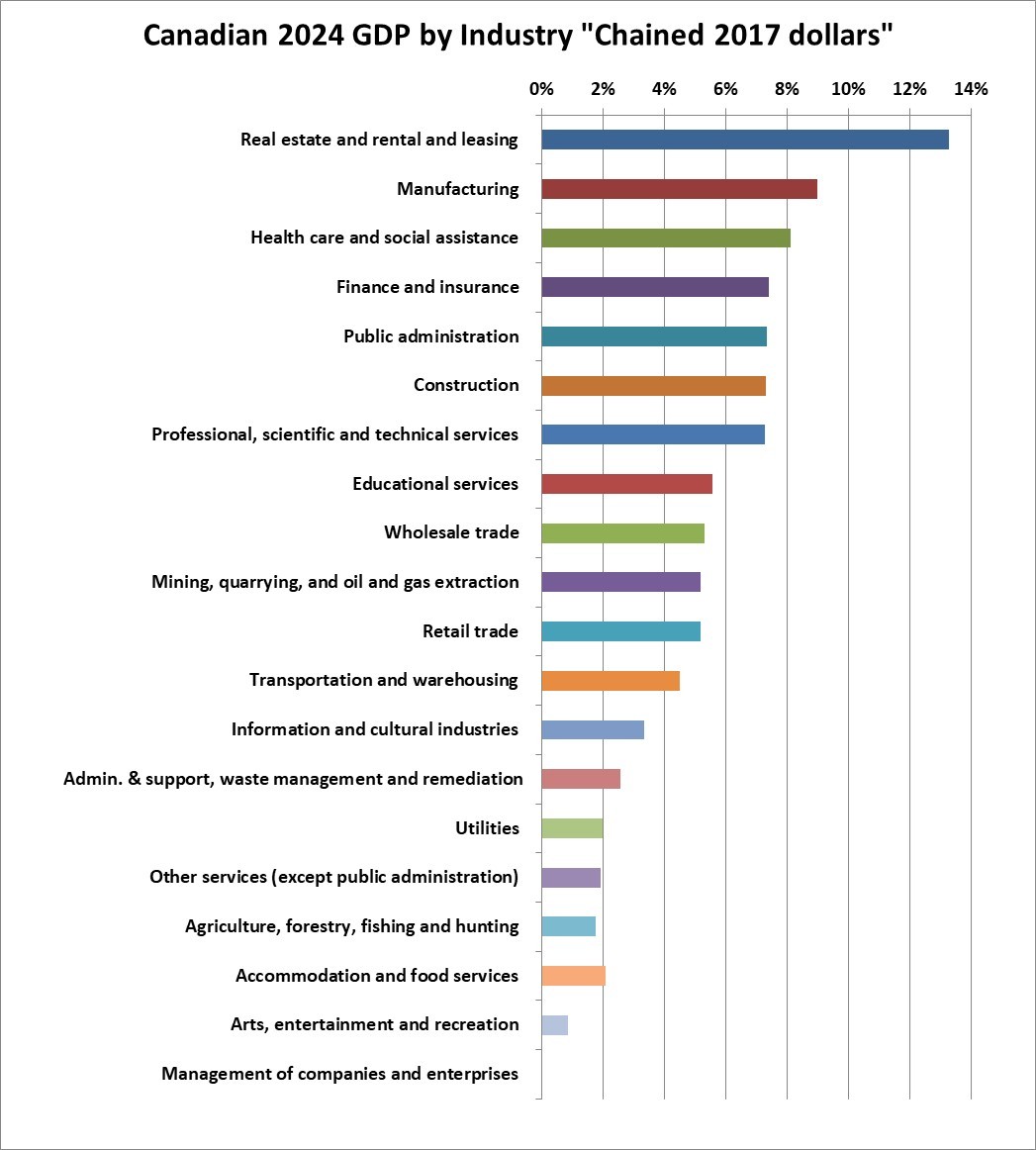

As of Q4 2024, Canada’s reported GDP per year, in 2024 dollars, was running at $3.135 trillion or $3,135 billion per year.

The following chart shows the percentage contribution of the various goods and services sectors to the total as of December 2024. Note however that this is based on something Statistics Canada calls 2017 chained dollars, which (I understand) basically assumes that there were no relative price changes among the sectors since 2017. I would prefer to use current dollars. However, for complicated reasons, Statistics Canada produces figures on GDP by industry in current dollars only on a three year lag basis. Chained dollars do a good job of measuring changes in volume or activity over time but may distort the relative contributions by segment in today’s dollars. This may be particularly true for commodity industries where price changes can be far different than the overall inflation level.

Data Source: Statistics Canada

https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=3610043403

The figures show that “Real estate and rental and leasing” is the largest segment of Canada’s economy at 13.2% of the total. This category (strangely) includes the “imputed” rental value of owner-occupied homes and that explains why this component is so very large. A large component here is the renting / leasing of real estate but it also includes auto and equipment leasing. Most retailers and office users rent their space. This category includes real estate brokers. Note that this category does not include constructing real estate! The high percentage related to the use of real estate (plus auto and equipment leasing) may seem high. But it includes the imputed rental value of owner occupied homes.

Manufacturing, while it may be lower than in years past, is still a very large portion of GDP and is the second largest component at 9.6%. Note that manufacturing includes process industries such as oil refineries, pulp mills and chemical plants.

Surprisingly, mining, quarrying, and oil and gas extraction has fallen down to the tenth largest item at 5.3% of total GDP. It would rank significantly higher than that in current dollars as opposed to 2017 chained dollars. The mining, quarrying and oil and gas extraction segment would rank higher in current dollars since oil prices were considerably higher in 2023 versus 2017.

Review the rest of the chart to see the composition of the Canadian economy and the percent contribution of different segments.

In total, goods-producing industries contributed for 26% of Canada’s GDP while service-producing industries contributed 74% of GDP. The public sector (which would be mostly or almost entirely service-producing) contributed 21% of the total GDP.

See the link to the source data just above to see the raw data if desired.

Who Consumes Canada’s GDP?

Canada’s 2023 GDP was consumed in the following fashion: (Q3 figures seasonally adjusted at annual rate)

Personal Household consumption: 59%

Government consumption: 22%

Investment in non-residential structures 8.5%

Investment in residential buildings 6.5%

Investment in intellectual property and inventory 2%

Government Investment: 4%

Net Exports: -2%

Total: 100%

When you hear that consumers “account” for most of Canada’s GDP, that does not mean that businesses account for little. In fact Businesses and (yes) government create the GDP and consumers consume the largest share. Government also consumes a large share but this is done to serve people (those same consumers) for example direct service in the case of education and health care and other direct services and indirect service in the case of police, the court, the army and other government services. This should not be considered surprising or alarming. Why else should things be produced except for consumption? (and for some investment to fuel future consumption).

A surprisingly large 21% of Canada’s GDP is expended on investment in (the creation of) longer lasting assets such as buildings (including houses) and equipment rather than being consumed for immediate gratification. This includes replacing and upgrading worn out buildings and assets which may account for it being so high.

END

Shawn Allen – shawn@investorsfriend.com

Investorsfriend Inc.

March 4, 2025