As many of you saw, I sent out an email today intended only for former (not current) customers. The email went to everyone on the free and paid lists by mistake. There was a link there to subscribe at a special price. If anyone who was not a current customer used the link that is completely fine.

It does create a bit of an issue where any existing paid customers used the link as they may end up with two subscriptions in PayPal. That can cause login problems as well as double billing. If you did that it’s fine except please understand we may have some issues to get through in regards to any billing or login problems.

If anyone has a big issue with some other people getting a special price, email and tell me what you would like done. I think the service is great value at the regular price and so I am hoping not too many people will be upset that someone else got a discount. But if you are just tell me what remedy you would like to see.

My apologies for the confusion created by the mis-directed email.

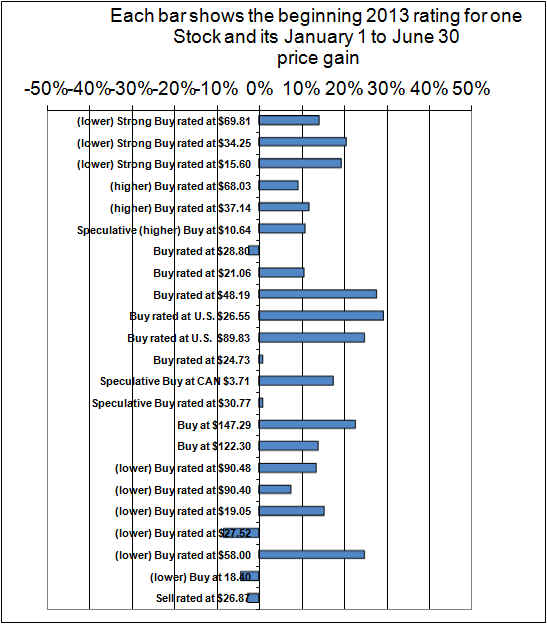

As you will see just below, one company on the list has been updated. And accordingly it is highlighted in yellow on the list. It will remain in yellow for about one month.

There had been a total lack of new updated reports in 2013 to date and that was related to the fact that basically everything had been freshly updated near the end of 2012. There have of course been comments about five days per week.

There has been a flurry of new subscribers due to some newspaper media coverage of my self and this site in Edmonton.

New subscribers should read the short article (the link to this article is also near the top of this page and many of you will have already reviewed it) with some information about using research page.

Occasionally people email to ask if I can review their portfolios. No, that is not a service we offer. InvestorsFriend Inc. and myself as its editor owner cannot give any personal advice. All of the advice here is generic. It’s not tied to anyone’s particular circumstances. Also, I also cannot comment on any stock or company not on the list here. My approach has always been that analysis must precede opinion. Unless I have analyzed a company in at least some detail I try to refrain from forming much less sharing an opinion. Analysis, of the sort that I undertake, cannot always prevent mistakes but it certainly helps.

Updates to the stocks on the list will come. I believe that over the course of several months or a year there will always be sufficient updates. Occasionally a new company will be added.

Boston Pizza Royalties Income Trust is updated and rated (lower) Buy at $19.96. In this case notice that it is not a corporation. This is actually a rather odd entity. A heavily financially engineered entity that collects a 4% royalty from food sales at Boston Pizza restaurants (excluded alcohol). The units unfortunately do not benefit in any meaningful way from new store openings. That is because new units are issued to basically the founders of BP in exchange for the right to the 4% from these new stores. The unit distribution will rise over time only if same store food sales rise. These units have bond-like characteristics but also offer some possible growth (and risk of shrinkage – and shrinkage is seldom or never a good thing!). Overall the 5.9% yield seems attractive given today’s low interest rates.

I own units and sometimes toy with the idea of selling as the price has risen. I have excellent gains on these units and so I worry about losing that gain. But overall it seems a good investment. If the unit price should fall due to perhaps a weak quarter or just lack of buying interest then I might buy more. If an investor is truly looking for yield and truly would not be bothered by a unit price decline as long as the cash distribution was unaffected then this might be good choice. But it is very hard to not be bothered by price declines. Those are always a risk.

Subscribers tell me they value me giving my though process. I probably should have bought more Boston Pizza even as the price rose. I believe I probably got (back) into this stock in the $11 something range. When I buy at $11 it simply becomes hard to buy later at say $13 or $15, much less $18 or $20. This is especially the case given that the share price did not rise because of any great earnings or dividend surge at all. To acknowledge that these units are still a (lower) Buy today at $20 is to admit that they were probably a steal at under $12 in 2010 rather than the Speculative Buy we rated it at. Even there we had to contend with our own history that called it a Strong Buy on December 13, 2008 at just $7.15. That was after it fell hard in the financial crisis, like everything. It would have been hard to keep calling it a Strong Buy after a swift rise the the $12 range. (I do try to make the ratings independent of past history but one can’t simply erase their memory of prior prices).

Although these units seem to be a reasonable investment, if one needs cash for other investments or purposes I certainly don’t see an issue with selling this one.

Our ratings history is:

Today (lower) Buy at $19.96

December 12, 2012 (lower) Buy at $19.05

May 13, 2012 Buy at $17.87

December 24, 2011 (higher) Buy at $14.18

November 28, 2010 Speculative (lower) Buy at $13.78.

May 16, 2010 Speculative Buy at $11.45

The difficulty in 2010 was that we knew the distribution would be sharply cut when it became taxable at the start of 2011. We also knew that the lower dividend would then be eligible for the dividend tax credit. But it certainly seemed a more risky situation given the then pending distribution cut.

November 28, 2009, Buy at (about) $11.40

August 15, 2009 (higher) Buy at $10.20

February 9, 2009 (higher) Buy at $8.65

December 13, 2008 Strong Buy at $7.15 (financial crisis, err… financial opportunity days)

Our initial rating was (lower) Buy at $14.47 on January 9, 2005.

We dropped it from the list in 2006 after our report got outdated and the price rose very steeply and I sold my units at a gain. It briefly soared to $20 in 2006 but we were not rating it at that time.

All this detail I got just from looking back at the links to my old comments. Anyone industrious can check it out if they wish. Just do searches for comments on Boston Pizza. For past years scroll to the bottom of this page for a link to past years’ comments. Of course there is always the risk that I backdated the old comments and ratings. Anyone who has the slightest suspicion of that should shop elsewhere for advice.