Report

COSCIENS Biopharma Inc. Report

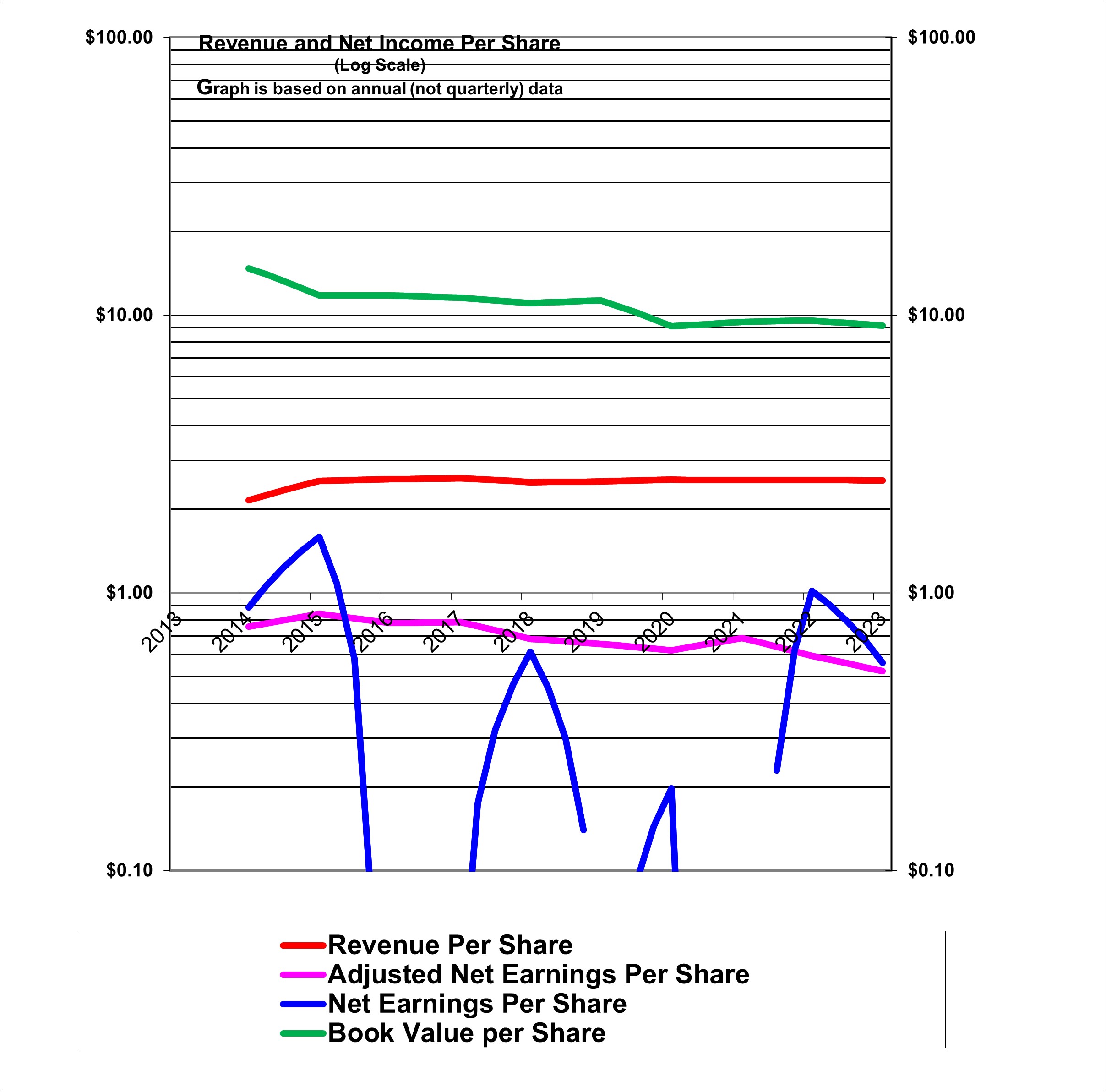

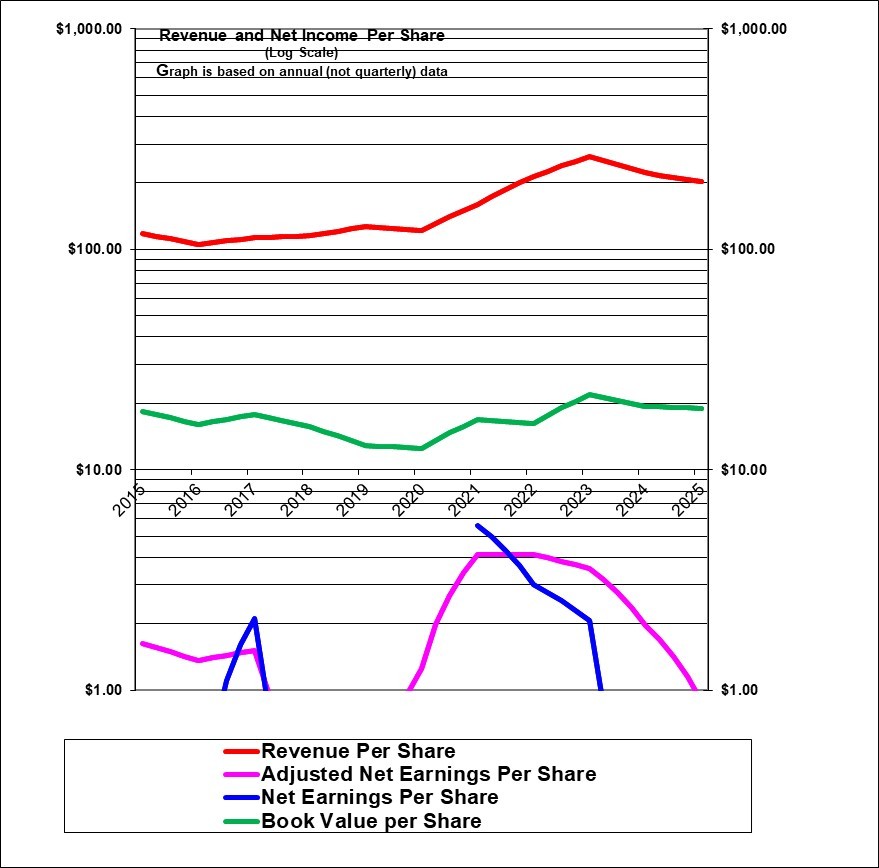

The graph here shows a history of failure, particularly recently. The company has lost so much money that’s book equity value per share has plummeted. Revenues have also plummeted. The promise here was that this was R&D biopharma company and that its research efforts would pay off. Instead, nothing has panned out.

Results had turned sharply downwards in 2017 and 2018 after a period of rapidly increasing revenues and especially earnings per share from 2013 to 2016. Revenue per share growth resumed in 2019. Earnings turned sharply higher in 2020, 2021 and 2022 But then revenues and especially earnings per sharp turned very sharply lower in the first nine months of 2023. The company is focused on investing in research and views its existing profitable base business which involves selling certain ingredients to the cosmetics industry as a way to fund its research into what it hopes will be more profitable products. The reason book value increased sharply back in 2016 but that was due to a share issuance at a price well above book value. To date its research has not panned out in anything commercial but it claims to have several promising irons in the fire. Now the company is proposing a merger with another company and this along with the revenue decline has very much clouded the outlook.

| Cosciens Biopharma Inc. (CSCI.TO) | |

| RESEARCH SUMMARY | |

| Report Author(s): | InvestorsFriend Inc. Analyst(s) |

| Author(s)’ disclosure of share ownership: | The Author(s) hold shares |

| Based on financials from: | Dec ’24 Y.E. + Q3 ’25 |

| Last updated: | December 12, 2025 |

| Share Price At Date of Last Update: | $ 2.09 |

| Currency: | $ U.S. for analysis but it trades in $ Canadian |

| Generic Rating (This rating does not consider the circumstances of any individual investor and is therefore not specific advice for any individual): | Highly Speculative Weak Sell at CAN $2.88 or U.S. $2.09 |

| Qualifies as a stock that could be bought with confidence to hold for 20 years? | No, it’s highly speculative |

| Has Wonderful Economics? | No |

| Has Excellent and Trustworthy Management? | Not certain |

| Likely to grow earnings per share at an attractive rate over the next decade? | Not certain |

| Positive near-term earnings outlook? | Unknown |

| Valuation? | Attractive but speculative |

| SUMMARY AND RATING: The graph a lot of volatility – earnings were sometimes negative including recently. The value ratios have deteriorated badly in recent years and would indicate a rating of Sell. Prior management has proven to be inept as virtually none of their many R&D efforts have panned out. The insider trading signal is neutral. Executive compensation now seems reasonable but was formerly excessive. The near term outlook is uncertain. This is a highly speculative Investment. We’ll give new management the benefit of the doubt and rate it a Highly speculative weak sell as opposed to Strong sell. It’s been a disaster. It does appear to have enough cash to struggle on for perhaps another two years waiting for better results. | |

| MACRO ENVIRONMENT: The macro environment such as interest rates and the state of the economy is probably not of much relevance to this company. | |

| LONG TERM VALUE CREATION: There has been huge long-term value destruction based on the share price. | |

| DESCRIPTION OF BUSINESS: Cosciens (formerly named Ceapro Inc.) is an Edmonton-based small “biotechnology company”. It has a line of existing cosmetic ingredient products (which it extracts from oats) which are profitable on their own but it formerly believed that its real value and future was in the products and processes it was researching and developing. There were quite a few R&D indicatives but most or possibly all have turned out to be worthless). It currently produces two ingredients for the cosmetics industry on a small commercial scale. It has one other product for a medical diagnosis but which failed tests in the U.S. and may or may not be worth anything although it is still be ing sold in Asia. It has developed (and/or purchased or licenced the rights to) certain proprietary and in some cases patented extraction and production technologies . Some of these are intended to produce commercially valuable methods to “deliver” a variety of drugs and treatments into the human body. They sell mostly (over 90%) through a single distributor and not by direct sales. The current products are used in the cosmetics and include an active ingredient in anti-aging skin creams. Brand names that contain Ceapro’s products include Neutrogena, Lubriderm, Aveeno, Jergens, Dove and others – We suspect its product is in one or a few but certainly not all or most of the products under these brand names. It indicates that it is the sole-source provider of ingredients in a number of products – but the purchasers can drive a hard bargain on price and the quantities needed are not large. | |

| ECONOMICS OF THE BUSINESS: The economics of its base business appear to be acceptable. But it has basically blown away its profits and most of its equity on various R&D initiatives which have mostly ended up being completely worthless. | |

| RISKS: This is difficult to know given recent major changes at the company. | |

| INSIDER TRADING / INSIDER Holding: There has been no recent insider trades in the public market. Therefore, the insider trading signal is neutral. | |

| WARREN BUFFETT’s CRITERIA: Buffett indicates that all investments must pass four key tests: the business is simple to understand and predict (Fail, because most investors would have no familiarity with the company’s products or its risks), has favorable long-term economics due to cost advantages or superior brand power (marginal pass), apparently able and trustworthy management (too early to tell with new management), a sensible price – below its intrinsic value (hard to say, this is entirely speculative), Other criteria that have been attributed to Buffett include: a low debt ratio (pass there is no debt), good recent profit history (fail) little chance of permanent loss of the investors capital (fail, given the poor track record) a low level of maintenance type capital spending required to maintain existing operations excluding growth (pass) Overall, the company does poorly on these tenets. | |

| MOST RECENT EARNINGS AND SALES TREND: Dismal with significantly lower revenues per share and negative earnings. | |

| COMPARABLE STORE SALES OR INDUSTRY SPECIFIC STATISTICS: Not applicable | |

| Earnings Growth Scenario and Justifiable P/E: With negative profits in the trailing year and plunging revenues earnings provide no guidance to valuation at this time. | |

| VALUE RATIOS: Analysed at a share price of U.S $2.88. As a research oriented company, value ratios provide only limited guidance and in theory understate the value. After several years of GAAP losses, the company was nicely profitable in 2020 and again in 2021 and 2022 but has now reported losses for several years along with plunging revenues. It could be argued that (most of) its research and development expenses are actually creating valuable assets and therefore are more in the nature of investments than expenses – however that research never ever seems to payoff despite many years of promises and more recently they have given up on much of their research efforts. The P/E is now negative as is the ROE! The price to book value ratio is, in isolation, acceptable at 1.80. There is no dividend. Overall the value ratios indicate a highly speculative company that should probably be rated a Strong Sell. | |

| TAXATION FOR SHARE OWNERS: Nothing unusual to note. | |

| SUPPORTING RESEARCH AND ANALYSIS | |

| Symbol and Exchange: | CSCI, Toronto covert to U.S |

| Currency: | $ Canadian |

| Contact: | czo@jtcir.com |

| Web-site: | www.ceapro.com |

| INCOME AND PRICE / EARNINGS RATIO ANALYSIS | |

| Latest four quarters annual sales $ millions: | $9.1 |

| Latest four quarters annual earnings $ millions: | $(14.9) |

| P/E ratio based on latest four quarters earnings: | negative |

| Latest four quarters annual earnings, adjusted, $ millions: | $(13.8) |

| BASIS OR SOURCE OF ADJUSTED EARNINGS: Starting 2019 added back 75% of other income or expense which is mostly foreign exchange gains / losses Previously added back 75% (assumes 25% income tax) of plant relocations costs and foreign exchange losses or gains also deducted large periodic tax credits. Deducted a large income tax recovery in 2015. In 2018 adjusted for a gain on litigation settlement and gains on deferred taxes. Starting 2021 we are usually no longer making any adjustments because the earnings are inherently volatile and there is no real value to making adjustments. Unusual legal costs are added back in 2023. These were likely associated with a proposed merger. | |

| Quality of Earnings Measurement and Persistence: Adjusted earnings have been volatile and positive in 2022 but then turned negative in the latest four quarters. Earnings may be under-stated due to the expensing of research and development. Non-refundable government grants are in some ways equivalent to earnings but are mostly accounted for as a reduction of capital costs or a reduction of research expenses. Cash flows in the past exceeded the earnings due the amortization of equipment and leasehold improvements as well as due to deferred income taxes in 2022. | |

| P/E ratio based on latest four quarters earnings, adjusted | negative |

| Latest fiscal year annual earnings: | $(15.3) |

| P/E ratio based on latest fiscal year earnings: | negative |

| Fiscal earnings adjusted: | $(15.3) |

| P/E ratio for fiscal earnings adjusted: | negative |

| Latest four quarters profit as percent of sales | -152.2% |

| Dividend Yield: | 0.0% |

| Price / Sales Ratio | 0.73 |

| BALANCE SHEET ITEMS | |

| Price to (diluted) book value ratio: | 1.31 |

| Balance Sheet: (as of Q3 2025) Assets are composed as follows: 41% is property and equipment (of which 26% is leasehold improvements and 30% is manufacturing equipment, 24% is equipment not yet available for use, and 19% is buildings) ,36% cash, 22% is other current assets (includes inventory, receivables and prepaid expenses). The assets are “financed” as follows:49% by the liability for a an unfunded pension plan that apparently resulted from their 2024 merger transaction), just 21% by equity 17% by current liabilities, and 13% by other liabilities. This is now a relatively weak balance sheet. The balance sheet has weakened considerably in the past few years. | |

| Quality of Net Assets (Book Equity Value): Relatively weak -see comments about the balance sheet composition. | |

| Number of Diluted common shares in millions: | 3.2 |

| Controlling Shareholder: No person or company owns as much as 10% of the shares and therefore the company is likely effectively controlled by management. | |

| Market Equity Capitalization (Value) $ millions: | $6.6 |

| Percentage of assets supported by common equity: (remainder is debt or other liabilities) | 21.3% |

| Interest-bearing debt as a percentage of common equity | 0% |

| Current assets / current liabilities: | 3.5 |

| Liquidity and capital structure: Adequate with no debt. | |

| RETURN ON EQUITY AND ON MARKET VALUE | |

| Latest four quarters adjusted (if applicable) net income return on average equity: | -109.8% |

| Latest fiscal year adjusted (if applicable) net income return on average equity: | -89.5% |

| Adjusted (if applicable) latest four quarters return on market capitalization: | -207.3% |

| GROWTH RATIOS, OUTLOOK and CALCULATED INTRINSIC VALUE PER SHARE | |

| 5 years compounded growth in sales/share | -6.3% |

| Volatility of sales growth per share: | Volatile and recently declining. |

| 5 Years compounded growth in earnings/share | negative past earnings |

| 5 years compounded growth in adjusted earnings per share | n.a. |

| Volatility of earnings growth: | Volatile, and recently negative. |

| Projected current year earnings $millions: | not available |

| Management projected price to earnings ratio: | not available |

| Over the last ten years, has this been a truly excellent company exhibiting strong and steady growth in revenues per share and in (adjusted) earnings per share? | No |

| Expected growth in EPS based on adjusted fiscal Return on equity times percent of earnings retained: | -89.5% |

| More conservative estimate of compounded growth in earnings per share over the forecast period: | 5.0% |

| More optimistic estimate of compounded growth in earnings per share over the forecast period: | 12.0% |

| OUTLOOK AND AMBITIONS FOR BUSINESS: Uncertain. The outlook for the existing base business which has been profitable has recently become quite clouded due to a huge revenue decline in recent years. | |

| LONG TERM PREDICTABILITY: Given the technologies and development risks involved, this is not a predictable company. | |

| Estimated present value per share: As this is an early-stage growth company it does not seem appropriate to attempt to forecast earnings. | |

| ADDITIONAL COMMENTS | |

| INDUSTRY ATTRACTIVENESS: (These comments reflect the industry and the company’s particular incumbent position within that industry segment.) Michael Porter of Harvard argues that an attractive industry is one where firms are somewhat protected from competition based on the following four tests. Barriers to entry (pass due to the science required) No issues with powerful suppliers (pass). No issues with dependence on powerful customers (fail as sales are over 90% to one key wholesaler who then sells to dozens of customers), No potential for substitute products (marginal pass) No tendency to compete ruinously on price (pass). Overall this industry (the base business) appears to be attractive to a successful incumbent in the industry – although the huge reliance on one wholesale customer is a definite concern. | |

| COMPETITIVE ADVANTAGE: Apparently little or nothing. | |

| COMPETITIVE POSITION: We did not see any information or discussion regarding its competitors or its market share. They have claimed they are the only supplier of some of their products. (Lately with their revenue plunge in the past few years that is coming into question.) | |

| RECENT EVENTS: The company has lost very significant money in the past two years. On December 1, 2025 the company announced an agreement for the commercialization of its Macrilen (macrilen) product in Hong Kong, Macao, Singapore and two provinces of Chine. This product is supposed to be a diagnosis tool for Human growth hormone deficiency but it failed its FDA tests in the U.S. In Q3 2025 the company gave up on its nutraceutical efforts as well as its line of cosmetic. It will focus on its two original products from yeas ago. In 2025 it reduced staff by about 27%. It also put in a new Board. It changed CEOs as Gilles Gagnon finally and left the company which is a very good thing. However a new CEO only lasted a few months. In a VERY big development, the company merged with TSX- and NASDAQ- listed Aeterna Zentaris. Ceapro would become a subsidiary of that company and existing Ceapro shareholders would own 50% of Aeterna. | |

| ACCOUNTING AND DISCLOSURE ISSUES: Historically, the disclosure was quite poor. In fact the company may have been misleading investors about its prospects for years. (Or perhaps management was simply delusional).It remains to be seen if this improves with the new management. | |

| COMMON SHARE STRUCTURE USED: Normal, one vote per share. | |

| MANAGEMENT QUALITY: With new management, this remains to be seen. Former management appears to have wasted million on research efforts that never panned out. | |

| Capital Allocation Skills: Historically this has been poor under former long-time CEO Gilles Gagnon who apparently wasted millions on numerous research projects that never panned out. | |

| EXECUTIVE COMPENSATION: Historically the compensation appeared to be excessive certainly for the CEO. At this time it appears to be more reasonable but, strangely, I could not see a summary compensation table int eh management circular. What I did see is that several executives were compensated in the range of U.S. 250,000. | |

| BOARD OF DIRECTORS: The current Board members may be the lone bright spot for this company. Three members have strong scientific knowledge and drug commercialization experience. Three others have strong investment management experience. Unfortunately, only one director owns shares. That director who recently became interim CEO owns about $750,000 Canadian dollars worth of shares and this MAY be enough to incent him to turn this company around. | |

| Basis and Limitations of Analysis: The following applies to all the companies rated. Conclusions are based largely on achieved earnings, balance sheet strength, achieved earnings per share growth trend and industry attractiveness. We undertake a relatively detailed analysis of the published financial statements including growth per share trends and our general view of the industry attractiveness and the company’s growth prospects. Despite this diligence our analysis is subject to limitations including the following examples. We have not met with management or discussed the long term earnings growth prospects with management. We have not reviewed all press releases. We typically have no special expertise or knowledge of the industry. | |

| DISCLAIMER: All stock ratings presented are “generic” in nature and do not take into account the unique circumstances and risk tolerance and risk capacity of any individual. The information presented is not a recommendation for any individual to buy or sell any security. The authors are not registered investment advisors and the information presented is not to be considered investment advice to any individual. The reader should consult a registered investment advisor or registered dealer prior to making any investment decision. For ease of writing style the newsletter and articles are often written in the first person. But, legally speaking, all information and opinions are provided by InvestorsFriend Inc. and not by the authors as individuals. The author(s) of this report may have a position, as disclosed in each report. The authors’ positions may subsequently change without notice. | |

| © Copyright: InvestorsFriend Inc. 1999 – 2025. All rights to format and content are reserved. | |

Melcor REIT report

Melcor Real Estate Investment Trust

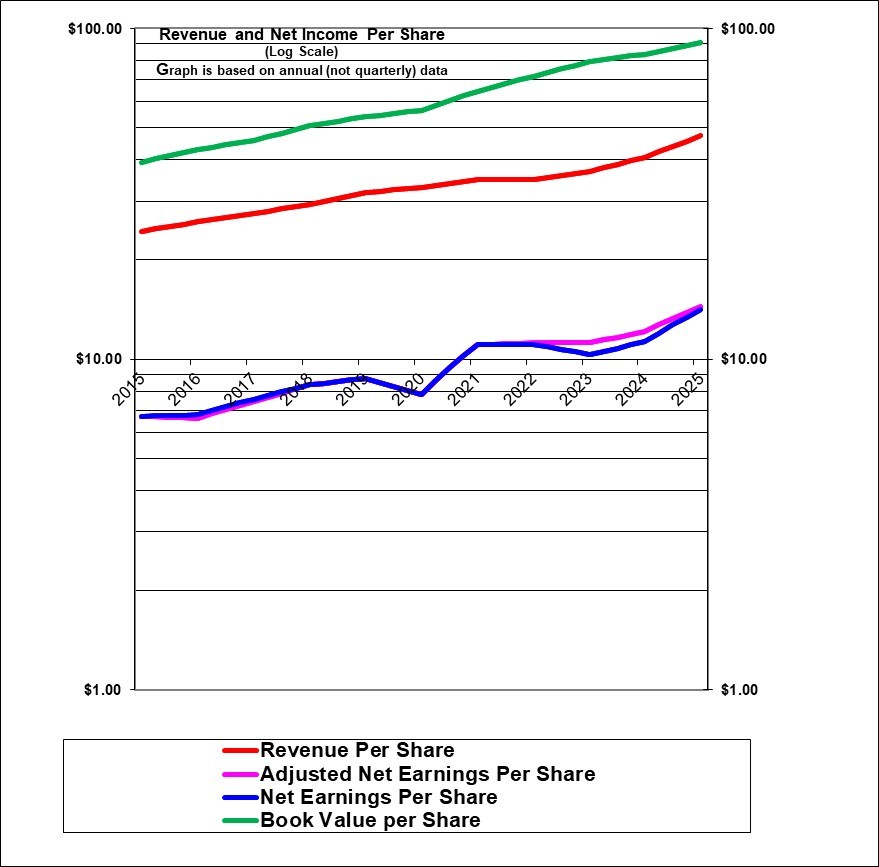

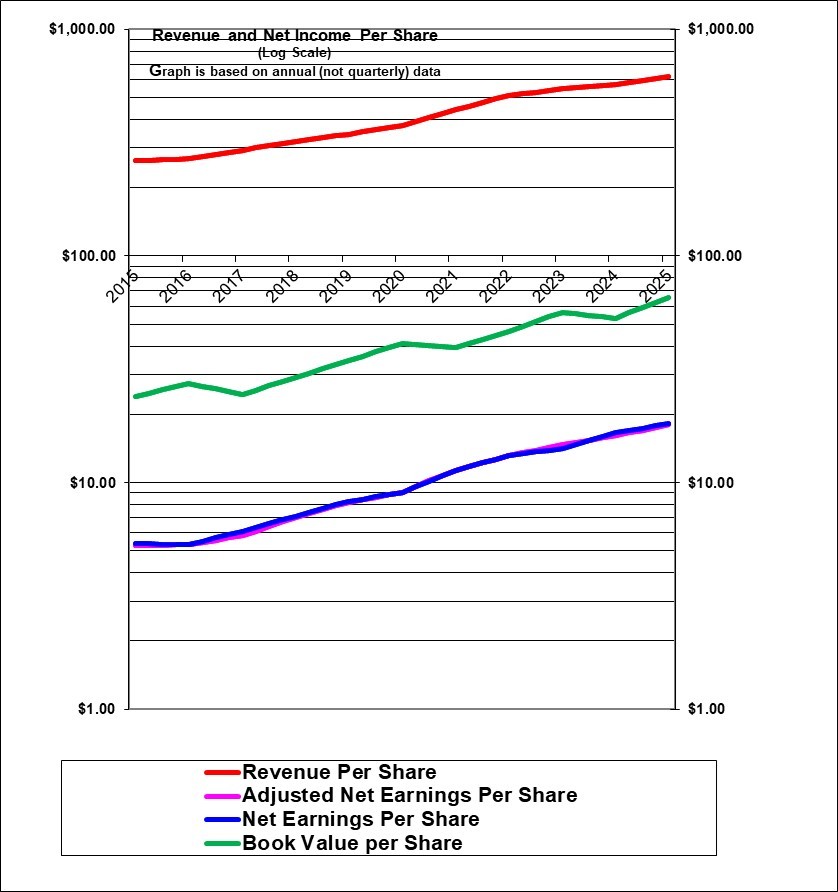

The top line, in green is the book value per unit. Ignore the initial higher value in 2014, it is not correct due to reasons related to the start up of the REIT that year. Since 2014 the book value per share has been declining somewhat due to market value losses on buildings due to the past recession conditions in Alberta and partly due to issuing units below book value. The 2020 decline in market values and therefore book value is due to the virus situation which led to market value declines on buildings. More recently in 2022 and 2023 the higher interest rates caused a modest decline in the calculated value of their buildings and this could certainly get worse or could have been worse as it depends on assumptions. Also the very high payout ratios of REITs always limits growth in book value.

Revenue per unit (the red line) has been relatively stable. Adjusted earnings which uses management’s figure for adjusted funds from operations has declined due to a combination of slightly higher vacancy rates (now more stable) and lower lease rental rates on renewals, and higher tenant incentives, all due to the past recession conditions in Alberta and also perhaps partly due to issues of units on a non-accretive basis. The adjusted earnings decline in 2020 was due to bad debt and rent forgiveness related to the virus situation. This improved substantially in 2021 and there was an extra increase due to a large lease termination fee. Earnings per unit (adjusted AFFO)declined 14% in 2022 due to higher expenses for utilities, professional fees, normalized capital expenditures and normalized tenant incentives and leasing commissions. There was an additional 12% decline in earnings per unit (adjusted AFFO) in 2023 mostly due to higher tenant incentive & leasing costs and higher interest rates.

The blue GAAP earnings per share line is totally meaningless due to IFRS accounting that (among other problems) treats the estimated gain or loss in market values of buildings as a current income or expense item (unlike traditional accounting did).There are also other market value gains and losses that come into income including large impacts related to the unit price.

| Melcor Real Estate Investment Trust (MR.UN, Toronto) | |

| RESEARCH SUMMARY | |

| Report Author(s): | InvestorsFriend Inc. Analyst(s) |

| Author(s)’ disclosure of share ownership: | The Author(s) do hold shares |

| Based on financials from: | Dec ’23 Y.E. |

| Last updated: | March 6, 2024 |

| Share Price At Date of Last Update: | $ 2.60 |

| Currency: | $ Canadian |

| Generic Rating (This rating does not consider the circumstances of any individual investor and is therefore not specific advice for any individual): | Speculative Buy at $2.60 |

| Qualifies as a stock that could be bought with confidence to hold for 20 years? | No |

| Has Wonderful Economics? | No |

| Has Excellent and Trustworthy Management? | Marginal |

| Likely to grow earnings per share at an attractive rate over the next decade? | No |

| Positive near-term earnings outlook? | No |

| Valuation? | Attractive but risky |

| SUMMARY AND RATING: The graph shows a decline in adjusted earnings per share over the years. Revenues per unit have been flat which is problematic as some expenses rose. Book value per unit has declined somewhat. The Value ratios (based on past earnings and the balance sheet) would support a rating of Speculative Buy due to the units trading at just 28% of book value but tempered by the low 5.6% ROE. The near-term and medium-term outlook is quite negative in terms of earnings due to higher interest rates that will cause market value losses on buildings as well as higher interest payment costs. Other costs are also rising but occupancy stable. Related to that the Macro Environment for Real Estate in general is poor. Management quality appears to be fair at best and certainly not great. The problematic vacancy rates in Office as well as the sharply higher interest rates were external factors. The insider trading signal is neutral. The business of owning commercial real estate (in general and not specific to Alberta) should be a stable business with acceptable but relatively low returns in the long term. The 38 properties are a mix of attractive newer retail but also some older strip malls. Much of the office portfolio is old and higher vacancies are a possibility as leases come to an end although renewals have been strong to date. The distribution has been suspended while the REIT undertakes a strategic review. There’s no guarantee but I suspect the review will be either neutral or noticeable beneficial to the unit price (currently $2.60). Overall, we now rate this as a Speculative Buy at $2.60. | |

| MACRO ENVIRONMENT: The recent sharply higher interest rates are very problematic. As of Q4 2023 only relatively modest market value losses have been booked and there could be more coming. Real Estate in general is now unpopular with investors due to higher interest rates. The outlook for office properties remains weak. The Alberta economy appears to be relatively strong and has seen significant population growth due to immigration. | |

| LONG TERM VALUE CREATION: (Updated Q4 2023) This REIT began trading eleven years ago in the Spring of 2013 with an IPO price of $10. The timing was not ideal given the recession in Alberta caused by sharply lower oil prices starting in 2014. It had paid an attractive yield of 6.75% annually on the $10 investment (but the distribution was temporarily reduced to 3.6% of that $10 IPO price and then partly restored to 4.8% and now has been suspended). But the market value of the units at $2.60 is well below book value and the unit price is about 74% below the IPO price. Therefore, to date, the REIT has provided a negative and very poor return for the IPO unit holders considering the distributions received minus the huge capital loss in the unit value. | |

| DESCRIPTION OF BUSINESS: (As of end of 2023) This Real Estate Investment Trust represents a 45% minority equity ownership in 38 income-producing (office, retail and some industrial) properties. The gross leasable area is 3.15 million square feet. All management and staff is effectively contracted out (mostly or entirely to the related majority 55% equity owner, Melcor Developments). The entity has no employees other than it appears the CEO and the part-time CFO who is shared with Melcor Developments. The Net rental income (for 2023) is 30% from office properties (20 buildings of low to medium rise largely in Alberta and with a concentration in Edmonton, some or most of these buildings are quite dated), 60% from retail properties (14 properties including 6 newer multi-building power centers and seven older neighbourhood shopping centers and one large Staples store/distribution center), 7% from 3 industrial properties and 2.4% from a land lease community (trailer home park). The office properties are 49% of the square footage but only 30% of net revenue and this appears to be due mostly to lower rent but partly due to higher vacancy. Geographically, 57% of the properties by net rental income are in Northern Alberta (Edmonton area plus Red Deer and Grande Prairie), 35% are in Southern Alberta (Calgary area plus Lethbridge) and 8% in Kelowna and Regina (which are now for sale). The majority of the office properties are older and less desirable buildings. The largest tenant is the government of Alberta at 5.8% of rent including health services with 8 locations in total. Tenants include (3 Shoppers Drugmart locations, 4 Royal bank branches, 3 Staples, 2 Ronas, 4 Canadian Brewhouse locations and 2 Michaels. | |

| ECONOMICS OF THE BUSINESS: This business generally provides relatively low returns (even with the use of substantial debt leverage) but the return is generally reasonably stable and reliable. We will assume that Adjusted Funds From Operations is a fair representation of the adjusted or economic earnings. On that basis the return on equity is quite modest at 5.6% as of the end of 2023 and appears to be heading lower. That is not an attractive return given the recent returns available of fixed income which rose sharply since the start of 2022. The business is heavily tied to the strength of the commercial business conditions in Alberta including vacancy rates in competing properties and the valuation is heavily affected by interest rates. | |

| RISKS: The biggest risks as of March 2024 are the ability to renew debt and the significant impact of higher interest rates. Profit is also likely to be pressured by higher utility costs. Market value losses on buildings are a definite risk due to higher interest rates and profit will also be impacted by higher interest rates, as well as other cost increases. It’s always possible that REITs could become subject to income tax like other businesses at some point. Another big risk is the outcome of the strategic review. It was meant to improve unit holder value so the output seems likely to be neutral (nothing comes of it) to positive (something good comes of it). | |

| INSIDER TRADING / INSIDER HOLDING: (Based on March 1, 2023 to March 6, 2024) The senior V.P. of investment properties, Randy Ferguson bought added a modest 250 units in March 2023 at $5.25 to hold a modest 775 units. Guy Pelletier, a Melcor Developments V.P. sold units at $4.60 in May 2023 to hold none. He also has a history of selling Melcor Development shares. Overall the insider trading signal is weak and could be considered neutral with one buyer and one seller. | |

| WARREN BUFFETT’s CRITERIA: Buffett indicates that all investments must pass four key tests: the business is simple to understand and predict (pass as the ownership of commercial office and retail rental property is a simple business especially for this REIT which is a pure ownership vehicle with management contracted out) has favorable long-term economics due to cost advantages or superior brand power (marginal pass as it is affiliated with a developer of properties that it can purchase at a slight discount but this is fundamentally usually a low return business), apparently able and trustworthy management (pass given their long-term record at Melcor Developments), a sensible price – below its intrinsic value (pass), Other criteria that have been attributed to Buffett include: a low debt ratio (fail, the debt level is a concern), good recent profit history (fail) little chance of permanent loss of the investors capital (probable pass) a low level of maintenance type capital spending required to maintain existing operations excluding growth (pass) | |

| MOST RECENT EARNINGS AND SALES TREND: Revenues per unit in the past four quarters starting with the most recent, being Q4 2023 have been very flat at down 1.6%, up 0.5%. down 0.2%,and up 0.2% and up 1.5%. In 2023 overall, revenues per unit were about unchanged. In 2022 overall, revenues per unit were unchanged. In 2021 overall, revenues per unit were down 0.4%. Adjusted earnings (AFFO) per unit in the past four quarters were up 1%, down 13%, down 6%, and down 25%. The figure for the full year 2023 was down 12% and for 2022 was down 14% and was up 11% in 2021 compared to the pandemic year of 2020 and assisted by a lease termination fee. The recent adjusted earnings trend (AFFO) is therefore quite negative primarily due higher tenant incentive and leasing costs, higher interest costs and higher normalized capital expenditures. | |

| INDUSTRY SPECIFIC STATISTICS: As of Q4 2023, the occupancy level is 87.6% down from 88.9 at Q3 and relatively flat in the past three years. This is significantly down from the 92.7% level of Q2 2017. Occupancy continues to be somewhat weak mostly due to a weak demand for its office space. But things are improving and the committed occupancy is 89% which is down from 91% indicated as of Q3.. | |

| Earnings Growth Scenario and Justifiable P/E: The trailing adjusted earnings P/E of 4.7 is apparently pricing in no growth but rather a decrease in earnings – which is very possible due to higher interest rates and inflation in other expenses. | |

| VALUE RATIOS: Based on a unit price of $2.60. Their is do yield as the distribution has been suspended due to a hopefully temporary cash crunch. The price to book value is calculated as just 0.28 and 0.72 on an enterprise (debt plus equity) basis. Our price to book value is calculated to include Melcor Development’s ownership. Note that the adjusted earnings is based on management’s view of adjusted funds from operations – which does appear to us to be a reasonable view of “true” earnings. The adjusted trailing P/E ratio appears very attractive (in isolation) at 5.0. The ROE is low and inadequate at 5.6%. The value ratios would support a Buy rating based on these trailing figures but note the concerns under outlook. | |

| TAXATION: With the distribution suspended only capital gains and loss tax impacts apply at this point. REITS do not qualify for the Canadian dividend tax credit. REIT distributions can be fully taxable as regular income or part of the distribution can be considered as a capital gain or as a return of capital. In the case of the MELCOR REIT, there has been a changing mix in how the distribution has been classified. On average more than half has been classified as return of capital. This creates some complexity for investors including tracking their adjusted cost basis. Holding these units in non-taxable accounts eliminates that complexity. | |

| SUPPORTING RESEARCH AND ANALYSIS | |

| Symbol and Exchange: | MR.UN, Toronto |

| Currency: | $ Canadian |

| Contact: | ir@melcorreit.ca |

| Web-site: | www.melcorreit.ca |

| INCOME AND PRICE / EARNINGS RATIO ANALYSIS | |

| Latest four quarters annual sales $ millions: | $73.9 |

| Latest four quarters annual earnings $ millions: | $16.3 |

| P/E ratio based on latest four quarters earnings: | 4.6 |

| Latest four quarters annual earnings, adjusted, $ millions: | $15.2 |

| BASIS OR SOURCE OF ADJUSTED EARNINGS: Uses management’s view of adjusted funds from operations. This appears somewhat conservative by deducting “straight line rent” accrual and possibly by deducting normalized capital expenditures which we understand are mostly recovered from tenants as part of recoverable operating expenses. | |

| Quality of Earnings Measurement and Persistence: The adjusted earnings figure appears to be reasonably measured. | |

| P/E ratio based on latest four quarters earnings, adjusted | 5.0 |

| Latest fiscal year annual earnings: | $16.3 |

| P/E ratio based on latest fiscal year earnings: | 4.6 |

| Fiscal earnings adjusted: | $15.2 |

| P/E ratio for fiscal earnings adjusted: | 5.0 |

| Latest four quarters profit as percent of sales | 20.5% |

| Dividend Yield: | 0.0% |

| Price / Sales Ratio | 1.02 |

| BALANCE SHEET ITEMS | |

| Price to (diluted) book value ratio: | 0.28 |

| Balance Sheet: (As of Q4 2024) Assets consist largely (90%) of investment properties. Plus another 5% representing 3 properties held for sale. These assets are valued at their estimated and modeled market value which is based on the value of expected future cash flows discounted at a market-based capitalization rate. An additional 4% are investments in tenant inducements (free leasehold improvements) and investments in lower rents in the early stages of rental contracts. The remaining 1% is mostly cash and short-term receivables and pre-paid amounts. It is essential to note and understand that the investment properties have been “marked” to recent modeled market value based on (as we understand it) the rental income less operating costs multiplied by an assumed market multiple that is typically paid to acquire net rental revenue. Or based on a forecast of future net rents and a terminal value discounted to present value. It is important to understand that the calculated (estimated) value of the properties changes (at least) annually and is subject to possible significant decline if the rents decrease due to vacancy or the market multiples or discount rates change due to factors including higher interest rates. This modeled market value may be higher than the actual price which could be obtained in the market especially at short notice. The original costs to construct and later improve the properties is not disclosed. These assets are financed as follows: 58% by debt, 38% by equity and the remaining 4% by tenant deposits and other minor liabilities. This is a somewhat weak balance sheet although it is supported by relatively reliable cash flows. | |

| Quality of Net Assets (Book Equity Value) Measurement: For this owner of commercial properties, the book value per share is an important valuation number. The book value of equity is subject to the estimated value of the buildings which itself is subject to changes with market conditions including interest rates, vacancy rates on the properties and vacancy rates on competing properties (which affect market rental rates). Such changes are then amplified by debt that is 1.5 times larger than the equity level. Overall, the book value per share is likely somewhat exaggerated as market value losses due to the recent higher interest rates have probably not yet been fully reflected. | |

| Number of Diluted common shares in millions: | 29.1 |

| Controlling Shareholder: The REIT is controlled by Melcor Developments which, in substance, owns about 55% of the REIT units. Melcor in turn is controlled by the Melton family. | |

| Market Equity Capitalization (Value) $ millions: | $75.6 |

| Percentage of assets supported by common equity: (remainder is debt or other liabilities) | 38.0% |

| Interest-bearing debt as a percentage of common equity | 153% |

| Current assets / current liabilities: | 0.3 |

| Liquidity and capital structure: Liquidity is very poor at this time. The REIT does not keep much cash on hand and so it is to a very good degree dependent on the kindness of its lenders. Melcor reports that lenders are cautious. A very significant amount of debt is due for renewal in the next two years. Management tells me that they CAN renew debt and the rates are not terrible. But they are unable to add to their debt even if needed. | |

| RETURN ON EQUITY AND ON MARKET VALUE | |

| Latest four quarters adjusted (if applicable) net income return on average equity: | 5.6% |

| Latest fiscal year adjusted (if applicable) net income return on average equity: | 5.6% |

| Adjusted (if applicable) latest four quarters return on market capitalization: | 20.1% |

| GROWTH RATIOS, OUTLOOK and CALCULATED INTRINSIC VALUE PER SHARE | |

| 5 years compounded growth in sales/share | 0.3% |

| Volatility of sales growth per share: | Stable |

| 5 Years compounded growth in earnings/share | -1.7% |

| 5 years compounded growth in adjusted earnings per share | -5.2% |

| Volatility of earnings growth: | Modest decline |

| Projected current year earnings $millions: | not available |

| Management projected price to earnings ratio: | not available |

| Over the last ten years, has this been a truly excellent company exhibiting strong and steady growth in revenues per share and in (adjusted) earnings per share? | No |

| Expected growth in EPS based on adjusted fiscal Return on equity times percent of earnings retained: | 5.6% |

| More conservative estimate of compounded growth in earnings per share over the forecast period: | -3.0% |

| More optimistic estimate of compounded growth in earnings per share over the forecast period: | 0.0% |

| OUTLOOK AND AMBITIONS FOR BUSINESS: There may be additional material market value losses on properties due to sharply higher interest rates. The average cap rate (which is a large determinant of building values) has increased only from 6.65% at the end of 2021 to 7.24% which could be a very inadequate increase given the sharp rise in interest rates. The outlook as of early March 2024 is for revenue per unit decreases as they sell assets to improve the balance sheet. The Alberta economy is relatively strong. But rent increases on retail properties could be offset by vacancies and/or lower rents on office properties plus the impacts of sold properties. Profit will be significantly impacted by higher interest rates on renewing debt in 2024 and recent renewals. Profit is also being negatively impacted by higher utility and admin costs. The normalized capex and tenant incentives have also increased in 2023 but may not increase any further in 2024. Overall, it seems very likely that adjusted earnings will decline further in 2024 . The outcome of the strategic review is very uncertain but could potentially lead to a higher unit price if the entire REIT is sold. The distribution may or may not be reinstated at some level by the end of 2024. | |

| LONG TERM PREDICTABILITY: For the next several years the predictability of cashflows appears to be threatened by higher interest rates. The predictability also depends to a large extent on the predictability of the Alberta commercial economy – but that appears to be strong. The REIT’s prospects also depend heavily on the level of surplus office and retail space that may develop near its buildings. There is some risk that older less desirable office space could face even higher vacancies as leases come to an end. The REIT believes it will eventually grow significantly due to purchasing buildings from Melcor Developments as Melcor constructs them (via contractors) and leases them up. But that prospect appears to be threatened now by the higher interest rates. | |

| Estimated present value per share: This calculation uses adjusted funds from operations (AFFO) per unit as the adjusted earnings figure. The future level of AFFO is very uncertain due to higher interest rates and higher costs. We calculate $2.56 if earnings per share (AFFO) shrink or 5 years at an average of 3% and the shares are then sold at a higher P/E of 8. And $4.46 if earnings per share (AFFO) remain flat and unchanged in 5 years and the shares are then sold at a P/E of 12. (This is not a share price prediction). In theory there should be growth if the distribution is not reinstated. This calculation assumes no distribution. Both estimates use a 7.0% required rate of return. | |

| ADDITIONAL COMMENTS | |

| INDUSTRY ATTRACTIVENESS: (These comments reflect the industry and the company’s particular incumbent position within that industry segment.) Michael Porter of Harvard argues that an attractive industry is one where firms are somewhat protected from competition based on the following four tests. Barriers to entry (marginal pass at best, there are few barriers to those wishing to purchase commercial rental property, however there may be little ability for anyone to construct new retail space at basically the same location as the REITs retail properties.). No issues with powerful suppliers (pass, as there are many buildings to be bought and many lenders). No issues with dependence on powerful customers (pass as there are many different tenants), No potential for substitute products (pass, space is needed – except that we have learned that office space may be replaced by work at home) No tendency to compete ruinously on price (fail as companies will tend to reduce rents very aggressively in times of surplus space given the fixed cost nature of the buildings). Overall this industry, based on these characteristics does not appear to be a particularly attractive industry even for established incumbents although it can be attractive when there is no surplus of rental space in the market. | |

| COMPETITIVE ADVANTAGE: Melcor REIT has the advantage of first access to properties developed by Melcor Developments. Because Melcor Developments avoids capital gains taxes on the sale to an affiliate and avoids real estate fees, it sells the properties to the REIT at a modest discount of 2 to 4%. It also has access to the economies of scale of Melcor Developments. This is not of any relevance as of 2023 and 2024 because the REIT is in no position to make any purchases. It likely has no particular advantages in attempting to market its space although it claims to provide superior service to tenants resulting in being a landlord of choice. | |

| COMPETITIVE POSITION: The Melcor REIT is a small player in a large and fragmented market. However, since property locations, especially retail locations, are not interchangeable, the REIT is not necessarily in a weak competitive position. But it has a weak balance sheet and a weak ability to access capital. And it is in a weaker position regarding Edmonton office properties (which are mostly in older buildings) since office tenants can move more easily than retail tenants. And the Edmonton office rental market is weak due to industry vacancies. | |

| RECENT EVENTS: The distribution has been suspended while the REIT undertakes a strategic review. Interest rates on debt have increased substantially and will continue to do so with upcoming debt renewals. Early in 2023 they renewed one mortgage at 5.69%. In Q3 renewed a small mortgage at 6.97% and three mortgages at (a hefty) 8.01%. There are significant renewals coming up in 2024 plus a large convertible bond due at the end of 2024. Tenant renewal incentives and leasing commissions have increased substantially. They currently have three strip mall centers for sale in Saskatchewan and are now looking to sell an office building in Kelowna and one in Lethbridge Alberta. They are doing this to reduce debt. In early 2023 they sold a building in Kelowna for $19.5 million and this was a market value gain of $4.3 million booked in 2022 and offsetting other market value losses. This was a good sign in terms of the true value of its assets but may have been very specific to Kelowna. In 2022 they recorded $16.3 million in modeled market value losses on other buildings for a net loss of $12 million. This was a modest loss given the interest rate hikes in 2022. The pandemic had led them to reduce the cash distribution per unit by 47% in 2020 in order to conserve cash. In early 2021 this was partly restored and then further restored in mid-2021 but the distribution remains 29% below the previous level. There was significant market value losses on properties in the past couple of years mostly due to more office space coming available in Edmonton which put some downward pressure on rental rates and also due to some increases in capitalization rates used in valuation. | |

| ACCOUNTING AND DISCLOSURE ISSUES: It appears that fair value changes on derivatives related to floating to fixed swaps and to the conversion option on debentures are now material adding to complexity. Accounting rules (which are no fault of the REIT) create some accounting complexities. The GAAP earnings figure is rendered completely meaningless due to the requirement to include the (modeled) market value changes of the properties in earnings, the lack of a depreciation expense, and the requirement to treat Melcor Development’s 55% ownership as a liability on the balance sheet and value the liability based on the unit price and to include the change in such valuation in GAAP earnings. In fact the GAAP earnings figure should be an embarrassment to the accounting regulator. Management appears to provide a reasonable figure to use as adjusted earnings which they refer to as adjusted funds from operations. This figure removes the impacts of changes in the market value of properties and the unit price and does include a deduction for normalized capital expenditures and normalized tenant incentives and leasing costs. The GAAP figure for book value per unit is also rendered meaningless by the accounting for Melcor’s ownership as a liability. We correct for this by treating that ownership as equity. In terms of disclosure we would like to see the age of the properties and the original dollars invested in each property since and including its construction or purchase by Melcor. Normally a REIT avoids income tax by distributing all of its taxable earnings. For 2022 the REIT had a gain for income tax purposes allocated to unit holders. For 2021, the REIT had a loss for income tax purposes probably due to Capital cost allowance. It appears there was a gain allocated to unit holders in 2020. Also a loss for income tax purposes each year back to 2017. There was a taxable income in 2016 and a large taxable loss in 2015. | |

| COMMON SHARE STRUCTURE USED: Generally normal, one vote per unit. But Melcor Developments the majority owner does have some special voting rights. | |

| MANAGEMENT QUALITY: Management appears to be somewhat weak. They may have been less than conservative through (arguably) an over-reliance on debt and lack of retained earnings although this is partly due to the rules by which REITs avoid income tax and partly due to investor expectations regarding REITs. | |

| Capital Allocation Skills: This remains to be seen. | |

| EXECUTIVE COMPENSATION: Technically, the REIT does not have any direct employees. The compensation for the two officers is from Melcor Developments and the REIT contributes to this indirectly through its management fee to Melcor Development. Compensation may be on the high side given the very weak performance. | |

| BOARD OF DIRECTORS: Warren Buffett has suggested that ideal Board members be owner-oriented, business-savvy, interested and financially independent. There are Seven Trustees. Three are Melcor Development appointees. All are well qualified. The independence of this Board has been improved in recent years. However, two Board members departed as of March 5 and replacements have not yet been named. | |

| Basis and Limitations of Analysis: The following applies to all the companies rated. Conclusions are based largely on achieved earnings, balance sheet strength, achieved earnings per share growth trend and industry attractiveness. We undertake a relatively detailed analysis of the published financial statements including growth per share trends and our general view of the industry attractiveness and the company’s growth prospects. Despite this diligence our analysis is subject to limitations including the following examples. We have not met with management or discussed the long term earnings growth prospects with management. We have not reviewed all press releases. We typically have no special expertise or knowledge of the industry. | |

| DISCLAIMER: All stock ratings presented are “generic” in nature and do not take into account the unique circumstances and risk tolerance and risk capacity of any individual. The information presented is not a recommendation for any individual to buy or sell any security. The authors are not registered investment advisors and the information presented is not to be considered investment advice to any individual. The reader should consult a registered investment advisor or registered dealer prior to making any investment decision. For ease of writing style the newsletter and articles are often written in the first person. But, legally speaking, all information and opinions are provided by InvestorsFriend Inc. and not by the authors as individuals. The author(s) of this report may have a position, as disclosed in each report. The authors’ positions may subsequently change without notice. | |

| © Copyright: InvestorsFriend Inc. 1999 – 2024. All rights to format and content are reserved. | |

Royal Bank of Canada Stock Report

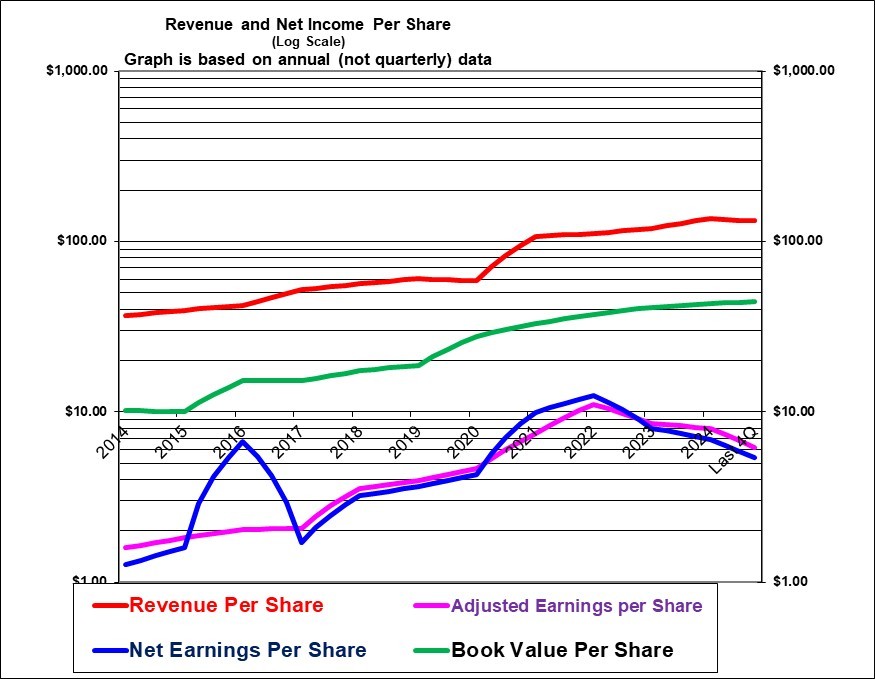

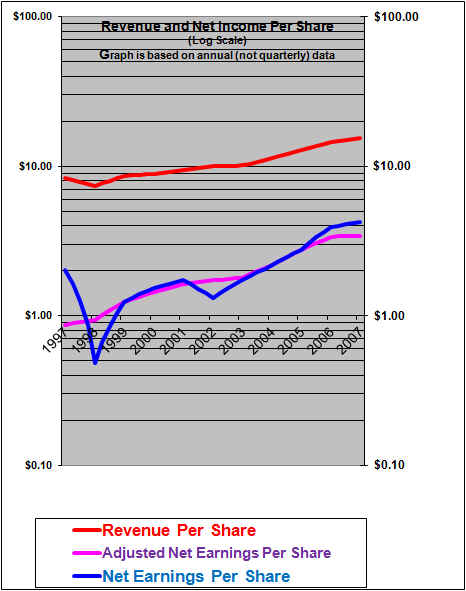

Royal Bank’s revenue per share (the red line) has grown at a relatively steady rate over the years, increasing at a compounded average of 6.9% per year in the period shown but with accelerated growth over the past few years. Earnings per share (the blue line) increased at a higher compounded average of 8.1% per year and with a sharp increase in the latest year. Book value per share has increased very steadily at a compounded average of 8.6% per year which is strong growth given that close to half the earnings are typically paid out as dividends and there has also been modest share repurchases.

| Royal Bank of Canada (RY, Toronto and U.S.) | |

| RESEARCH SUMMARY | |

| Report Author(s): | InvestorsFriend Inc. Analyst(s) |

| Author(s)’ disclosure of share ownership: | The Author(s) hold shares |

| Based on financials from: | Oct. ’25 Y.E. +Q1 ’26 |

| Last updated: | February 27, 2026 |

| Share Price At Date of Last Update: | $ 228.00 |

| Currency: | $ Canadian |

| Generic Rating (This rating does not consider the circumstances of any individual investor and is therefore not specific advice for any individual): | Weak Buy / Hold at CAN $228 |

| Qualifies as a stock that could be bought with confidence to hold for 20 years? | Yes! |

| Has Wonderful Economics? | Yes |

| Has Excellent and Trustworthy Management? | Yes |

| Likely to grow earnings per share at an attractive rate over the next decade? | Yes |

| Positive near-term earnings outlook? | Probably yes |

| Valuation? | Neutral |

| SUMMARY AND RATING: The graph of revenues per share (red line) shows strong and relatively steady historic growth with a noticeable surge in 2025 on top of strong growth in 2024. The earnings per share line shows quite strong growth over the years but with an earnings decline in 2020 primarily due to estimated loan losses caused by the pandemic. There was a noticeable surge in 2025. The Value ratios would support a rating of Weak Buy to Buy. Management quality appears strong. The insider trading signal is moderately negative. Executive compensation is high but not a concern given the size of this bank. The outlook or objective indicated by RBC is for Earnings per share growth of 7% plus in the next three to five years. RBC has strong economics and some strong competitive advantages in terms of its scale and established market position. It appears to be a business that can reliably predicted to continue to grow over the years. RBC, however (like all banks) is highly leveraged and therefore there is some small risk of very major problems in certain scenarios. There are also potential risks associated with lower housing prices and a slow resale housing market and mark to market losses on some investments. Overall RBC is a consistent money maker but achieves this with high leverage which is managed through a finely tuned risk management system. Noting that its valuation in relation to earnings, book value and dividends are all at the higher end of their range and that earnings jumped in 2025, it may be a time for caution. Overall our rating is Weak Buy / Hold. | |

| MACRO ENVIROMENT: Higher loan losses, a slower home market and the U.S. tariff issues are headwinds. | |

| LONG TERM VALUE CREATION: Royal Bank has created excellent value in the long term. | |

| DESCRIPTION OF BUSINESS: Last updated Q4, 2023 and Q2 2024 . Royal Bank of Canada is the country’s largest bank with assets of $2.03 trillion dollars, a common equity market cap of $207 billion dollars, 1247 bank branches, 4341 automated teller machines and 94,000 employees in 29 countries. Earnings by segment as of Q2 2024 were 53% from personal and commercial banking (in Canada, the U.S. and the Caribbean) [And 68% of the revenue in this personal & commercial segment is Canadian personal banking] , 28% from capital markets (includes equity and debt origination and distribution, and structuring and trading), 14% from wealth management – down from 20% in 2019 (mainly Canada, the U.S., the U.K, the channel islands and Asia), 5% from insurance (In Canada and reinsurance outside Canada). The return on equity for personal and commercial banking is reported at a stunningly profitable 28% and this high level has been sustained for years! (The high ROE is presumably due to massive leverage on CMHC mortgages as well as lucrative fees), 10% ROE for wealth management, 37% ROE for insurance (which seems extraordinarily high but might be explained by selling high margin insurance like life insurance on mortgages and by reinsurance which will likely occasionally have losses), and 15% ROE in capital markets (similar to the 13% of 2018). Overall corporate ROE was 14%. Based on 2017 figures Canada accounts for 61% of revenue, The U.S. accounts for 23% of revenue, International (37 countries) accounts for 17% of revenue. For 2019 (and 2018), 57% of revenue is from non-interest income (investment management fees, account service charges, foreign exchange fees and card fees, insurance, underwriting and trading) and 43% from net interest income. Interestingly, RBC has very little (only 5%) of its Personal and Commercial banking outside of Canada but its Wealth Management business in the U.S. is almost twice as large as its Canadian wealth management level. | |

| ECONOMICS OF THE BUSINESS: (Updated as of Q1 2023) RBC’s economics are strong. It does however like most banks depend on very high (even extraordinarily high) leverage. Its profit as a percent of revenue was recently 31%. However that translates into a profit on (ending) assets of only 0.83% as revenue is only 3% as large as the assets. This 0.83% return on ending assets was then leveraged up to 15.9% return on ending equity as ending common equity was only 524% as large as the assets (The common equity is extremely highly leveraged – which is typical for banks). The high ROE indicates that the economics of the business are very good but it is achieved through massive leverage which can be risky. The economics are also strong in that the business is of a recurring nature and the customers tend to be “sticky”. | |

| RISKS: See annual report for a full discussion of risks. Data breaches are a definite risk. New disruptive technologies are a possible risk. Banks always run the risk that borrowers will fail to pay their loans. This risk is increased by the very large leverage of most banks and of Royal Bank in particular. However, the bank has in place numerous and complex risk management strategies that are designed to prevent its risks from creating any major financial problems for the bank. Share owners must place their faith in management and its risk management abilities. RBC has operations in tax havens including the Caribbean, and (of more concern) the Channel islands and Luxemburg. It could face risks in that area if it is found to be helping customers evade income taxes. As of 2023 there are added risks in regard to bad loans due to borrowers struggling with higher interest rates and due to a projected mild recession. | |

| INSIDER TRADING / INSIDER HOLDING: Based on February 1, 2025 to February 27, 2026: Five insiders, including the CEO, sold shares after exercising options. In two cases very substantial number of shares. Two other insiders sold a small number of shares Most insiders were holding and not selling (which is positive). Overall, the insider trading signal is moderately negative. In the past insiders were buying “under a plan”, that was not the case in the past year for whatever reason./ RBC itself bought back share regularly over the year apparently with no regard to the price. | |

| WARREN BUFFETT’s CRITERIA: Buffett indicates that all investments must pass four key tests: the business is simple to understand and predict (marginal pass because the various sectors and geographies make RBC more complex and particularly because it is very hard to judge the risk of this highly leveraged business), has favorable long-term economics due to cost advantages or superior brand power (pass due to scale and established history of high ROE achievement), apparently able and trustworthy management (pass), a sensible price – below its intrinsic value (marginal pass), Other criteria that have been attributed to Buffett include: a low debt ratio (arguably a fail given the massive leverage although that is not unusual in banking), good recent profit history (pass) little chance of permanent loss of the investors capital (pass – although with high leverage there is some risk) a low level of maintenance type capital spending required to maintain existing operations excluding growth (pass). | |

| MOST RECENT EARNINGS AND SALES TREND: The earnings growth is sometimes distorted by volatile swings in the allowance for credit losses which are NOT adjusted for in adjusted earnings. Banks strangely deduct interest expense in arriving at Revenue. Revenue per share growth in the past four quarters beginning with the most recent (Q1, 2026) was 8%, 15%, 17% and 11%. Adjusted earnings per share (sometimes affected by volatile estimates for credit losses) were 13%, 26%, 18% and 7%. In 2025, overall revenues per share were 16%! and adjusted earnings per share growth was 19%. In 2024, overall revenues per share were up 10 and adjusted earnings per share were up 8%. In 2023, overall revenues per share were up 5% but adjusted earnings per share were unchanged. In 2022, overall revenues per share were flat while adjusted earnings per share were up just 1%. Overall, the recent earnings trend is very strong in the latest year in particular. In 2021 overall the earnings per share were up by a huge 42% but a large part of that was loan loss reversals and revenues per share were up 5.5%.. In 2020 overall, the earnings per share growth was a decline of 11% (mostly due to estimated pandemic loan losses) and revenue per share declined 2% partly due to lower interest margins. In 2019 overall, the earnings per share growth was 5% and revenue per share growth was 9%. In 2018 overall, the earnings per share growth was 13% (possibly boosted by the Trump tax cuts) and revenue per share growth was 6%. In 2017 overall, the earnings per share growth was 12% and revenue per share growth was 6%. | |

| INDUSTRY SPECIFIC STATISTICS: In Q1 2026, the provision for credit loss was 0.41%. For fiscal 2025, the provision for credit loss was 0.43%. For fiscal 2024, the provision for credit loss was 0.35%. For fiscal 2023, the provision for credit loss was 0.29%. For fiscal 2022, the provision for credit loss at 0.06% was abnormally low. For fiscal 2021 Provision for Credit Loss was negative 0.10% as they reversed loss estimates from 2020 which was a hefty 0.63% due to the pandemic and was sharp increase from 2019 at 0.31% and 2018 at 0.23%. Gross impaired loans at Q1 2026 was 0.86%. At end of 2025 was 0.83% and at end of 2024 was 0.59%. Gross Impaired Loans in 2022 were just 0.26% and in 2021 were 0.31% down from 0.47% in 2020 and 2019. In Q1 2026 Net interest margin in the personal sector was 2.66% up from 2.50% a year earlier. In Q1 in commercial lending it was 3.93% up from 3.89% the prior year. Net interest margin in the personal and commercial sector in 2023 was 2.74%. Net Interest Margin on average earning assets was 1.62% in 2025, 1.54% in 2024. 1.50% in 2023 in 2022 was 1.48% and in 2021 was 1.28% down from 1.55% 2020 and 2019 was 1.61% and 2018 was 1.64% on average earning assets. | |

| Earnings Growth Scenario and Justifiable P/E: With a dividend yield of 2.9%, and a P/E of 15.3% it is pricing in growth in the range of about 7%. | |

| VALUE RATIOS: Analysed at Canadian $228 (U.S. $167). The price to book value ratio at 2.50 unattractively high because it is at the higher end of its historic range. Although it could be considered reasonable given the high 16.7% ROE. The trailing P/E ratio is not unreasonably high but is higher than normal for a bank. The dividend yield is reasonably attractive at 2.9% although it is at the lower end of its historic range and amounts to a payout of 44% of earnings. The Return on equity is quite high at 16.7% which is similar to its long-term average. Earnings per share have grown at a compounded average of 13.1% in the past five fiscal years but that is from the low 2020 figure and the ten year growth is 8.1% and revenue per share has grown at a compounded average of 7.4% in the five years and 6.9% in the ten year period. This is good revenue growth considering that about half of earnings are normally paid out as dividends. We calculate the intrinsic value to be $185 per share if earnings can be expected to grow at 4% per year and the P/E declines to 12 and (more optimistically) $252 if earnings per share grow at 8% per year for five years and the P/E falls modestly to 14. These intrinsic value calculations use a required return of 7.0%. These value ratios support a rating of Weak Buy to Buy. | |

| TAXATION: Nothing unusual. | |

| SUPPORTING RESEARCH AND ANALYSIS | |

| Symbol and Exchange: | Royal Bank of Canada |

| Currency: | $ Canadian |

| Contact: | invesrel@rbc.com |

| Web-site: | www.rbc.com/investorrelations |

| INCOME AND PRICE / EARNINGS RATIO ANALYSIS | |

| Latest four quarters annual sales $ millions: | $67,826.0 |

| Latest four quarters annual earnings $ millions: | $20,500.0 |

| P/E ratio based on latest four quarters earnings: | 15.7 |

| Latest four quarters annual earnings, adjusted, $ millions: | $20,954.0 |

| BASIS OR SOURCE OF ADJUSTED EARNINGS: For the most recent few periods we have used a new adjusted earnings figure provided by management. They likely started doing this because of an usual retroactive tax hit in Q1 2023. Prior to that we had not made any adjustments except for a gain on a sale in 2017 and 2016. Loan loss estimated can also be quite volatile but we did not adjust for that. | |

| Quality of Earnings Measurement and Persistence: Earnings measurement is probably of reasonably high quality but there are certainly some estimates involved such as for loan losses. Some mark to market changes in asset values flow to the net income. | |

| P/E ratio based on latest four quarters earnings, adjusted | 15.3 |

| Latest fiscal year annual earnings: | $19,868.0 |

| P/E ratio based on latest fiscal year earnings: | 16.2 |

| Fiscal earnings adjusted: | $20,369.0 |

| P/E ratio for fiscal earnings adjusted: | 15.8 |

| Latest four quarters profit as percent of sales | 30.9% |

| Dividend Yield: | 2.9% |

| Price / Sales Ratio | 4.73 |

| BALANCE SHEET ITEMS | |

| Price to (diluted) book value ratio: | 2.48 |

| Balance Sheet: (Updated Q2, 2024) The composition of assets is as follows: 47% of assets are loans (of which 63% are categorized as retail and 37% as wholesale), 15% assets purchased under reverse repurchase agreements and securities borrowed (essentially short term secured lending and 93% of this is offset by assets sold under similar arrangements that appear to be like short-term deposits much of which are 1 to 6 month terms.), 20% securities – which would mostly pay a cash yield or interest so are like loans but highly liquid (42% of which are held for trading and 58% are held for investment), 6% derivatives (which appear to be mainly for risk management purposes and are fully offset by derivative liabilities), 5% “other” – which is mostly financial receivables and 5% cash and deposits with other banks, and less than 1% goodwill. Liabilities consist of 65% deposits (of which 38% are personal, 60% are business and government and 2% from other banks), 7% derivatives, 14% obligations for assets sold under repurchase agreements (essentially short-term borrowing or perhaps equivalent to a very short-term deposit where the “depositor” has security – the great majority of these are under 1 month.), 1.6% obligations related to securities sold short, 6% “other” – which is mostly financial payables of various kinds, 5.5% common equity, 0.7% subordinated debt and 0.5% preferred shares. In general the balance sheet shows some complexity in that loans are only 47% of assets (62% if assets purchased under repurchase agreements are treated as loans). Common equity at about 5.5% is very highly leveraged which is typical of banks. | |

| Quality of Net Assets (Book Equity Value) Measurement: It is difficult to judge the reliability of the net book value. Not all assets are marked to market and the leverage is so high that a small error in asset values could wipe out a large chunk of equity. On the other hand most of the assets are very liquid and a significant portion are marked to market. | |

| Number of Diluted common shares in millions: | 1,401.9 |

| Controlling Shareholder: No one is allowed to own more than 10% of the shares. | |

| Market Equity Capitalization (Value) $ millions: | $319,629.6 |

| Percentage of assets supported by common equity: (remainder is debt or other liabilities) | 5.5% |

| Interest-bearing debt as a percentage of common equity | 9% |

| Current assets / current liabilities: | not revealed |

| Liquidity and capital structure: With common equity of only 5.5% of the asset level (albeit higher than recent years), the capital structure appears to be weak in that regard. But this is apparently typical for large banks. And, the assets are considered to be highly liquid and safe and credit rating agencies (S&P) rate the debt at A. On a risk-weighted basis and by bank standards it balance sheet is considered strong. | |

| RETURN ON EQUITY AND ON MARKET VALUE | |

| Latest four quarters adjusted (if applicable) net income return on average equity: | 16.7% |

| Latest fiscal year adjusted (if applicable) net income return on average equity: | 16.6% |

| Adjusted (if applicable) latest four quarters return on market capitalization: | 6.6% |

| GROWTH RATIOS, OUTLOOK and CALCULATED INTRINSIC VALUE PER SHARE | |

| 5 years compounded growth in sales/share | 7.4% |

| Volatility of sales growth per share: | strong, steady growth |

| 5 Years compounded growth in earnings/share | 12.5% |

| 5 years compounded growth in adjusted earnings per share | 13.1% |

| Volatility of earnings growth: | moderately volatile |

| Projected current year earnings $millions: | not available |

| Management projected price to earnings ratio: | not available |

| Over the last ten years, has this been a truly excellent company exhibiting strong and steady growth in revenues per share and in (adjusted) earnings per share? | Yes |

| Expected growth in EPS based on adjusted fiscal Return on equity times percent of earnings retained: | 9.3% |

| More conservative estimate of compounded growth in earnings per share over the forecast period: | 4.0% |

| More optimistic estimate of compounded growth in earnings per share over the forecast period: | 8.0% |

| OUTLOOK AND AMBITIONS FOR BUSINESS: RBC is projecting continued growth in the next 3 to 5 years but at the objective of 7%+ EPS growth it would be significantly lower than the 19% gain in 2025. Loan losses are still increasing but have not been problematic. There is also possible headwinds in terms of mark to market losses on investments and loan losses on non-CHMC mortgages. The reinsurance business can occasionally lead to material losses. But overall the future looks bright. | |

| LONG TERM PREDICTABILITY: Royal Bank of Canada has been growing its assets and earnings per share for decades. It seems reasonable to assume that it can continue to grow with the economy. But it is possible though that newer technologies will disrupt banking leading to lower profits. Technology is allowing for big cost reductions as transactions become more and more digital and self-serve. | |

| Estimated present value per share: We calculate $185 if adjusted earnings per share grow for 5 years at the more conservative rate of 4% and the shares can then be sold at a lower P/E of 12 and $252 if adjusted earnings per share grow at the more optimistic rate of 8% for 5 years and the shares can then be sold at a moderately lower P/E of 14. Both estimates use a 7.0% required rate of return. | |

| ADDITIONAL COMMENTS | |

| INDUSTRY ATTRACTIVENESS: (These comments reflect the industry and the company’s particular incumbent position within that industry segment.) Michael Porter of Harvard argues that an attractive industry is one where firms are somewhat protected from competition based on the following four tests. Barriers to entry (Pass, there are certainly barriers to achieving a large scale in banking since it is difficult to acquire customers although new entrants are emerging and could become a concern in future). No issues with powerful suppliers (pass). No issues with dependence on powerful customers (pass), No potential for substitute products (pass) No tendency to compete ruinously on price (marginal pass – they may compete aggressively on some products but there are some parts of the business where there appears to be little price competition such as credit card rates and currency exchange rate fees.). Overall this industry appears to be attractive for an established large incumbent. | |

| COMPETITIVE ADVANTAGE: Size and scale are advantages. Customers find it inconvenient to switch banks and therefore having an established large market share is an advantage. They indicate that there are significant barriers to entry in the reinsurance part of their business. | |

| COMPETITIVE POSITION: Royal Bank is the largest Bank in Canada. In personal and commercial banking it is number 1 or 2 in all key product categories. It has a very strong competitive position in Canada and competes effectively in certain U.S. and European lines of business.2025 CEO letter states that RBC is number 1 in market share in Canada in all it’s major segments except insurance. RBC entered 2026 as the 11th largest bank globally and 6th largest in North America by market cap. | |

| RECENT EVENTS: RBC has relatively recently completed the $13.5 billion acquisition of HSBC Canada it’s largest acquisition ever (apparently bigger than the City National acquisition of several years ago). Also acquired a wealth management business in the U.K called Brewin Dolphin. | |

| ACCOUNTING AND DISCLOSURE ISSUES: The disclosure of large banks is voluminous. But we are always left with some questions. They measure revenue after deducting interest expense. They speak of trading revenues but it is often impossible to know if they refer to proprietary trading for their own account or merely collecting fees on customer trading activity, which is a vastly different thing. Net income is mostly reported in a legal but misleading way. They fail to prominently show on the actual income statement and focus the lower net income to common after deducting preferred share dividends and non-controlling interest. Accounting rules require gains on asset sales to be counted as revenue, which distorts the figure. Earnings are impacted by mark-to market changes in some assets and liabilities. Currency changes affect earnings. They did not show normalised earnings for the unusually high credit loss reserves in 2020 or the negative estimated loans losses in 2021 which would have been quite useful. | |

| COMMON SHARE STRUCTURE USED: Normal, one vote per share. | |

| MANAGEMENT QUALITY: Overall, the management quality appears to be very high. | |

| Capital Allocation Skills: Given the high ROEs in all of the various divisions of the Bank, capital allocation skills appear to be very strong based on past results. | |

| EXECUTIVE COMPENSATION: Updated with April 2020 figures. Compensation is generous but given the size of the bank and its earnings, this is not a concern. | |

| BOARD OF DIRECTORS:(Updated 2024) Warren Buffett has suggested that ideal Board members be owner-oriented, business-savvy, interested and financially independent. The Board members at RBC are well qualified. Most are independently relatively wealthy and hold more shares than the minimum target of $750k. A number of the members are quite recent and none have been in place since before 2005 and the average tenure is only about 5 years. We’d like to see a bit more continuity that that. | |

| Basis and Limitations of Analysis: The following applies to all the companies rated. Conclusions are based largely on achieved earnings, balance sheet strength, achieved earnings per share growth trend and industry attractiveness. We undertake a relatively detailed analysis of the published financial statements including growth per share trends and our general view of the industry attractiveness and the company’s growth prospects. Despite this diligence our analysis is subject to limitations including the following examples. We have not met with management or discussed the long term earnings growth prospects with management. We have not reviewed all press releases. We typically have no special expertise or knowledge of the industry. | |

| DISCLAIMER: All stock ratings presented are “generic” in nature and do not take into account the unique circumstances and risk tolerance and risk capacity of any individual. The information presented is not a recommendation for any individual to buy or sell any security. The authors are not registered investment advisors and the information presented is not to be considered investment advice to any individual. The reader should consult a registered investment advisor or registered dealer prior to making any investment decision. For ease of writing style the newsletter and articles are often written in the first person. But, legally speaking, all information and opinions are provided by InvestorsFriend Inc. and not by the authors as individuals. The author(s) of this report may have a position, as disclosed in each report. The authors’ positions may subsequently change without notice. | |

| © Copyright: InvestorsFriend Inc. 1999 – 2026. All rights to format and content are reserved. | |

Utility Cost of Capital Presentation

Click the arrows on the presentation to move from slide to slide or click the PDF version.

This regulated (cost of service) utility cost of capital presentation is intended to be of use for:

Utility regulation Commission / Board panel members

Commission / Board staff members

Utility staff involved in regulated utility cost of capital matters

Customer representatives in utility rate cases

Question or comments can be sent to shawn@investorsfriend.com

Shawn Allen developed this presentation over a period of many years working in the field of regulated utility cost of capital.

The material in this presentation may be shared in any forum, with appropriate attribution to the source.

Topics include:

Definition of “capital” for regulated utilities and legal requirements for a fair return

How to determine the fair return on debt for regulated utilities

How to set the equity ratio for regulated utilities

How to set the fair return on equity for regulated cutilities

And additional topics

TFI International Stock Report

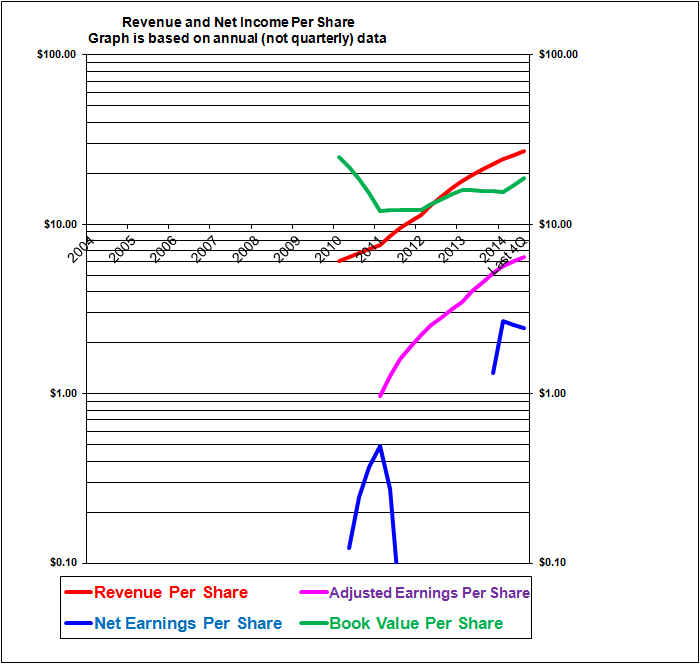

This chart shows very strong historic growth but with an earnings decline in the past three years due to a weak freight market and made worse by the tariff war with thye U.S. 2026 is predicted to show an improvement as growth will likely ultimately resume for this well-managed company.

| TFI International Inc. (TFII, Toronto) | |

| RESEARCH SUMMARY | |

| Report Author(s): | InvestorsFriend Inc. Analyst(s) |

| Author(s)’ disclosure of share ownership: | The Author(s) hold shares |

| Based on financials from: | Dec ’24 Y.E. +Q3 ’25 |

| Last updated: | November 22, 2025 |

| Share Price At Date of Last Update: | $ 121.19 |

| Currency: | $ Canadian |

| Generic Rating (This rating does not consider the circumstances of any individual investor and is therefore not specific advice for any individual): | Buy at $121 |

| Qualifies as a stock that could be bought with confidence to hold for 20 years? | Yes |

| Has Wonderful Economics? | Yes, despite price competition |

| Has Excellent and Trustworthy Management? | Yes! |

| Likely to grow earnings per share at an attractive rate over the next decade? | Yes |

| Positive near-term earnings outlook? | Q4 2025 will be weak with some recovery in 2026 |

| Valuation? | Attractive |